")

Calculator Template")

: What It Is and How to Calculate")

Performing accounts payable reconciliation is a crucial financial process often overshadowed by bank reconciliation and accounts receivable reconciliations during the month-end close. This neglect can expose companies to potential errors and fraud.

Skipping accounts payable reconciliations leaves an organization vulnerable, unable to detect errors such as bill duplication or misdirected payments. The repercussions extend beyond internal discrepancies, affecting supplier relationships, trade credit eligibility, and opportunities for advantageous rates and early payment discounts.

This blog aims to shed light on the significance of accounts payable reconciliation and its process and explore how automation can empower businesses to navigate this financial terrain.

What is Accounts Payable Reconciliation?

Accounts payable reconciliation is the process of comparing and verifying a company’s accounts payable records with external documents to ensure accuracy and completeness. The reconciliation process typically includes matching the invoice sent by the vendor with the company’s ledger and purchase order. The primary goal is to confirm that the company’s financial records align with the vendor’s invoice.

Here are the key documents typically involved in the accounts payable reconciliation process:

- Invoices: Original invoices from suppliers detailing the goods or services provided, along with the agreed-upon prices and payment terms.

- Purchase Orders (POs): Documents issued by the buyer to the seller outlining the specifics of the products or services to be purchased, including quantities and prices.

- Delivery Receipts: Confirmation that goods or services have been received, and signed by an authorized person within the company.

- Vendor Statements: Summaries sent by vendors detailing the transactions, payments, and outstanding balances between the company and the vendor.

- Check Copies or Payment Confirmations: Records of payments made to vendors, including check copies, electronic payment confirmations, or other proof of payment.

- General Ledger: The company’s primary accounting record, summarizing all financial transactions, including accounts payable entries.

- Bank Statements: Reconciliation may involve cross-checking transactions in the accounts payable ledger with those in the company’s bank statements.

- Accruals and Prepayments: Documentation related to any adjustments for accruals or prepayments that need to be considered in the reconciliation.

- Correspondence with Vendors: Any communication with vendors regarding discrepancies, refunds, or adjustments.

Why is Accounts Payable Reconciliation Important?

Reconciling accounts payable is crucial for accurate financial tracking, especially at the close of each business year. This process allows businesses to precisely determine their expenditures, facilitating the calculation of profits and expenses.

Beyond the financial bottom line, accounts payable reconciliation serves as a valuable tool for scrutinizing business spending. It offers an opportunity to identify and eliminate unnecessary purchases, contributing to cost efficiency.

Neglecting regular accounts payable reconciliation intervals can lead to significant discrepancies between bank statements, purchase orders, and vendor invoices. This mismatch may result in missing or unrecognized entries, causing financial losses for the company.

Moreover, the absence of an accounts payable reconciliation system leaves businesses vulnerable to inflated invoices from vendors. Without this scrutiny, hidden costs and overcharges may go unnoticed, leading to blind payments and potential financial losses. Therefore, implementing a regular accounts payable reconciliation process is an effective practice to ensure transparency and financial accuracy before making any payments.

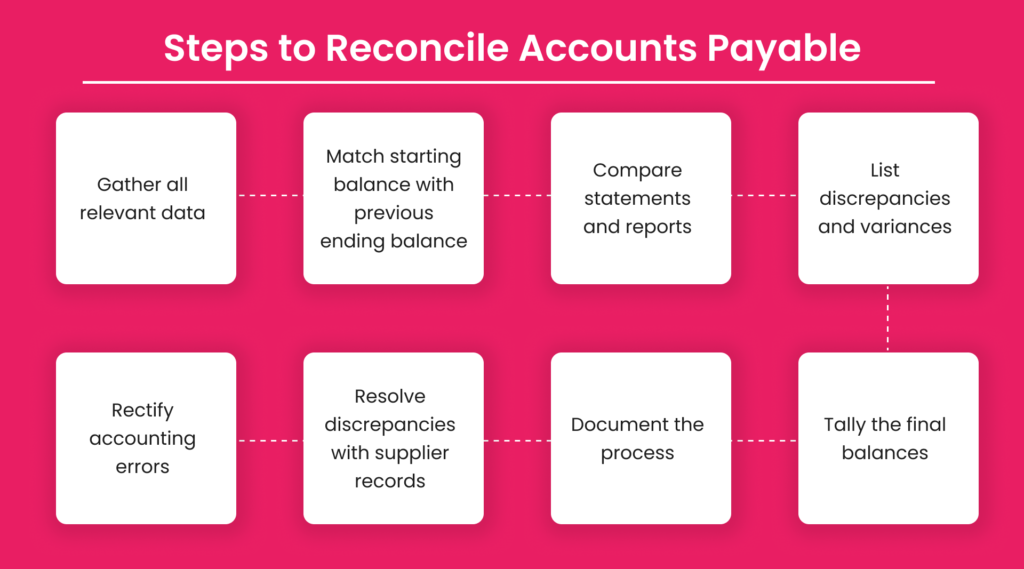

Steps to Reconcile Accounts Payable

The reconciliation process may vary from business to business but here are the key steps:

1. Gather all relevant data

Assemble crucial information for reconciliation, including supplier statements, the accounts payable ledger, and aging reports. These documents outline outstanding amounts, payments, and credit notes. All these statements should be for the same accounting period. A company dealing only with one or two vendors may not have to create the AP aging but, it’s a must for tracking current liabilities when you’re dealing with several vendors.

2. Match the starting balance with the previous ending balance

Confirm that the current period’s starting balance matches the previous period’s ending balance. If the AP balances don’t match, find the last accounting period when these balances matched. Start reconciling accounts payable from that period onwards but isolate and identify the discrepancy from prior periods.

3. Compare statements and reports

Compare supplier statements with the general ledger and accounts payable aging report. A successful match concludes the reconciliation; otherwise, investigate unmatched items.

4. List discrepancies and variances

Check for variance between accounting records and supplier statements. Scrutinize original invoices, purchase orders, delivery reports, and vouchers to pinpoint the cause of discrepancies.

5. Rectify accounting errors

Correct the accounting errors such as unrecorded purchases, returns, adjustments for returned checks, or data entry mistakes that were identified during the reconciliation.

6. Resolve discrepancies with supplier records

Discrepancies identified during AP reconciliation may be due to an error with the supplier’s records. If there are items you can’t solve on your own, get in touch with your supplier to discuss the discrepancies. Document ongoing investigations within the reconciliation report.

7. Document the Process

Record details of the reconciliation process, particularly if further investigation is necessary. While carrying unresolved items to the next period is less than ideal, prioritize their resolution.

8. Tally the final balances

To complete the process, you will have to tally the debit and credit sides of the accounts payable ledger. The credit side consists of outstanding bills and invoices for credit purchases, while the debit side reflects paid invoices. So, ultimately the credit balance of the AP general ledger would be the summarization of those invoice amounts that are due.

9 Best Practices for a Successful Accounts Payable Reconciliation

Embrace Automation

Opt for automated tools to streamline the accounts payable reconciliation process. Automation minimizes manual errors and enhances efficiency by swiftly matching invoices with purchase orders and receipts.

Prioritize Regular and Timely Reconciliation

Conduct monthly or quarterly reconciliations to promptly identify and rectify discrepancies. Regular checks prevent the accumulation of long-standing errors that can become challenging to address.

Emphasize Documentation and Record-Keeping

Maintain organized records of invoices, purchase orders, and receipts. Proper documentation simplifies reconciliation processes and supports audit activities.

Standardize Workflow

Establish a standardized workflow for accounts payable reconciliation to ensure consistency and reduce the likelihood of errors. Consider implementing automation software that aligns with your team’s workflow.

Implement Three-Way Matching

Adopt a three-way matching system reconciling purchase orders, invoices, and receiving notes. This thorough approach minimizes errors by ensuring consistency across all relevant documents.

Conduct Duplicate Invoice Checks

Develop a process to identify and eliminate duplicate invoices, preventing inadvertent overpayments. Vigilance is crucial, especially when dealing with recurring invoices from multiple vendors.

Stay on Top of Payments

Monitor outstanding payments to identify and address overdue invoices, fostering strong vendor relationships. Some accounts payable reconciliation software facilitates auto-disbursement to avoid late penalties.

Conduct Audits and Strengthen Internal Controls

Regularly perform internal audits to ensure compliance with reconciliation procedures and strengthen internal controls. Address any identified weaknesses proactively to enhance security.

Prioritize Vendor Relationship Management

Leverage software tools to streamline payment and communication processes with vendors. Effective vendor relationship management extends beyond reconciliation, fostering stronger partnerships and potential benefits like improved payment terms and discounts.

How Often Should You Reconcile Accounts Payable?

Typically, the accounts payable reconciliation process takes place after a reporting period. Some business experts recommend at least annual reconciliations, while others, recognizing the importance of timely financial oversight, suggest more frequent sessions—perhaps allocating a workday each month for the task.

While daily reconciliations would be ideal, especially for businesses with high transaction volumes, this may not be practical for those still reliant on manual accounts payable operations. For the freedom to conduct reconciliations at their desired frequency, businesses are increasingly turning to AP automation software, which can efficiently manage the process on their behalf.

Challenges of the Manual Reconciliation Process

1. Prone to Errors

The manual accounts payable reconciliation process is susceptible to human errors, such as data entry mistakes and miscalculations. These inaccuracies can lead to discrepancies in financial records, impacting the overall accuracy of the reconciliation.

2. Time-Consuming Nature

Manual reconciliation is a time-intensive task, demanding substantial efforts in comparing various documents like invoices and purchase orders. The prolonged duration required for this process can hinder operational efficiency and delay financial reporting.

3. Limited Scalability

As businesses grow, the volume of transactions and paperwork in accounts payable increases. Manual reconciliation struggles to scale efficiently, making it challenging for companies to manage larger workloads without a proportional increase in resources.

4. Increased Vulnerability to Fraud

Manual processes lack robust checks and balances, making them more susceptible to fraudulent activities. Without automated safeguards, unauthorized transactions or manipulations can occur, posing a significant risk to the integrity of financial data.

5. Compliance Challenges

Adhering to regulatory and compliance requirements is crucial for businesses. Manual accounts payable reconciliation may struggle to consistently meet these standards, potentially leading to non-compliance issues and associated penalties. Adopting automated solutions can enhance accuracy and regulatory adherence.

Benefits of Automating Accounts Payable Reconciliation Process

Listed below are a few of the benefits of implementing automation in the accounts payable reconciliation process:

- AP automation reduces time spent on manual tasks such as data entry, matching, and approval, allowing the finance team to focus on strategic activities.

- Automation lowers the risk of human error in data entry and reconciliation thus, enhancing the integrity of financial records.

- AP automation minimizes operational expenses, facilitates the utilization of early payment discounts, and avoids late payment penalties, leading to cost savings.

- Automation provides real-time visibility into AP processes, ensuring transparency and control.

- Automation enforces compliance with company policies and regulatory requirements.

- Automated approval workflows speed up invoice processing, enabling quicker payments.

- Automation enhances vendor relationships by providing accurate records and audit trails contributing to trust and collaboration.

- AP automation software includes robust security features, protecting both the company’s and vendor’s important data.

- AP automation can scale with business growth, adapting to increased transaction volumes.

- Allows integration with accounting software to sync and export data.

- Eliminates the need to wait for manually generated reports, providing constant access to analytics.

The adoption of automation in accounting processes proves invaluable, saving significant time and effort for your accounting team. Modern accounts payable software, equipped with advanced capabilities, can swiftly perform reconciliations in seconds. However, the challenges extend beyond reconciliation preparation, especially during month-end procedures. Accounting teams often find themselves burdened with extensive data entry tasks before diving into reconciliation and generating month-end reports.

In a manual AP process, precious work hours are dedicated to mundane data entry and manual expense categorization, tasks that could be efficiently handled by OCR and machine learning technologies. To streamline and enhance the entire accounts payable reconciliation process, consider the implementation of Peakflo’s Automated Reconciliation solution. The innovative solution offers a seamless and efficient approach, eliminating the burdens associated with manual tasks and empowering the accounting team to focus on more strategic and value-driven activities.

FAQ

How often should you be doing accounts payable reconciliation?

The frequency of accounts payable reconciliation depends on the complexity and scale of your organization, its financial transactions, and the number of vendors it pays. Smaller, less complex organizations can typically reconcile their accounts payable once a month. However, larger organizations with multiple departments and numerous vendors may need to reconcile more frequently—twice a month or even weekly—to reduce errors that can accumulate over time.

Does automation reconcile transactions in real time?

Financial automation platforms, like Peakflo, offer seamless integrations with accounting software that can auto-sync daily. This means any changes made in one system will automatically update in the other, providing near-real-time reconciliation, though not constant.

Is bank reconciliation part of the accounts payable reconciliation process?

Yes, bank reconciliation is a crucial part of the accounts payable reconciliation process. It focuses on your organization’s cash accounts and transactions, comparing your internal cash records against your bank’s records for that account. This process helps explain the differences between your bank statement balance and your ledger cash balance.

{kind=link}