")

Calculator Template")

: What It Is and How to Calculate")

Handling employee travel reimbursements can feel like navigating a maze, especially when tax implications come into play. Determining which expenses are taxable and which are not can confuse many businesses. Are the meals deductible? What about mileage?

The stakes are high, and one misstep could result in compliance issues or an audit. Employers and employees often struggle with unclear documentation and shifting IRS guidelines, so understanding how to handle these reimbursements correctly is essential.

This article will break down the essentials of handling employee travel reimbursements, from key tax rules to understanding which expenses are taxable. Whether you are an employer looking for compliance or an employee seeking clarity, this guide will walk you through common pain points, avoiding costly mistakes, and the importance of proper documentation.

Overview of Employee Travel Reimbursements

Handling travel reimbursements goes beyond covering costs. Employers must get it right for tax purposes. But how can you make the process simple while staying compliant?

Learn to recognize the difference between personal and business travel expenses.

In a nutshell:

- Deductible expenses are business-related costs like airfare, lodging, and meals during a work trip. These can be claimed as tax deductions.

- Non-deductible expenses are personal costs, such as entertainment or extra amenities, which cannot be claimed for tax deductions.

This helps you understand when a reimbursement might trigger taxes.

- How are Travel Expenses Treated for Tax Purposes When Reimbursed by Employers

Travel expenses are taxed mainly by the type of expense and how it is reimbursed. Here is how:

- Accountable Plans: Reimbursements are tax-free if they follow a proper plan. This means:

- The expenses must be for business purposes.

- They must be documented with receipts.

- Any excess amount needs to be returned.

- Personal vs. Business: Personal travel expenses are always taxable, while strictly business-related travel can be tax-free if supported by proper records.

- Excessive Reimbursements: If an employee receives more than necessary or cannot provide adequate proof, the extra reimbursement is taxed as income.

- Focus on Federal Tax Implications

Understanding the federal tax implications of travel reimbursements is crucial. Take a look at the following employee travel expense reimbursement guidelines to understand the concept better:

- IRS Safe Harbor: Reimbursements under an IRS-approved “accountable plan” are not taxable to employees.

- Taxable Reimbursements: If an employer uses a non-accountable plan, those payments are taxed and must be reported on the employee’s W-2 form.

- Per Diem Rates: Meal and lodging reimbursements that follow the IRS per diem guidelines stay non-taxable. Exceeding these rates results in taxable income.

What Are the Reimbursable Travel Expenses?

Reimbursable travel expenses cover costs employees incur during business trips. Understanding which expenses qualify ensures accurate claims and smooth reimbursement processes, helping employees manage costs without financial strain.

- Transportation Expenses

Transportation costs are the first essential expense that needs reimbursement. This includes all transportation used during a business trip, such as train or flight tickets, public transport, car rentals, or ride shares. Employees must submit official documentation of their travel expenditures, such as copies of their tickets or payment receipts.

- Accommodation Expenses

Accommodation costs are also part of business travel reimbursements. This covers hotel charges, valet or parking fees, internet charges, and SIM card costs. Set expense limits to help employees stay within the budget and avoid overspending.

- Business-Related Entertainment Expenses

Business-related entertainment costs are also eligible for reimbursement. These expenses include social events, concerts, or dinner parties to engage clients or potential clients. Employees who spend money on food, drinks, or other refreshments for clients are also reimbursed.

- Meal Expenses

Employees can claim reimbursement for meals they purchase during a business trip. This includes meals for themselves or their clients. Daily meals may also fall under the per diem allowance, a daily allowance for traveling employees.

- Incidental Expenses

Incidental expenses cover minor travel costs, such as room service, tips for hotel staff, gifts for clients, or laundry services. Such costs are reimbursable after the trip.

What Are the Steps of a Travel Reimbursement Process?

A simple travel reimbursement process saves time and avoids confusion. By following each step; employees can submit accurate claims while finance teams ensure quick approvals, keeping both sides satisfied and stress-free.

Step 1: Pre-Travel Approval

Before travel expenses are reimbursed, employees need approval. They must submit a request with trip details, like destination, dates, purpose, and budget. Your company should use a simple request template or system for travel approvals.

Step 2: Expense Guidelines and Policies

After an employee submits a travel request, the company reviews it. You then provide them with expense guidelines, a list of reimbursable costs, and the approved budget, which helps them understand what they can claim.

Step 3: Expense Documentation

Employees need to keep records of every expense during their trip. This means saving receipts for meals, client events, tickets, and hotel stays. These receipts are required for reimbursement claims.

Step 4: Expense Report Preparation

After the trip, employees create a report listing all expenses, including amounts and categories. They attach receipts, and the finance team checks the report for accuracy.

Step 5: Review and Approval

The finance team reviews each claim, comparing receipts with the reported amounts. This ensures that all expenses are valid and meet company rules. They confirm every expense has proof before approval.

Step 6: Reimbursement Processing

Once approved, the reimbursement is processed. The amount is usually added to the employee’s paycheck.

Step 7: Reconciliation and Reporting

After reimbursement, the expense details are added to accounting records. The team rechecks everything and reconciles the expenses. A final report keeps track of all costs for accurate records.

Key Scenarios for Travel Expense Deductions

Specific scenarios determine whether travel expenses are deductible and reimbursements can remain tax-free. Understanding and adhering to these rules by automating travel and expense reporting can prevent mistakes leading to later tax issues.

1. Travel Expenses Must Be Ordinary and Necessary

The IRS states that travel expenses must be “ordinary and necessary” to be deductible. Ordinary means the cost is common and accepted in your line of work, while necessary implies that it is helpful or appropriate for the business.

For example, a flight to meet a client in another city would typically qualify, as it is an ordinary and necessary part of business. However, extravagant costs like luxury suites or first-class tickets beyond what is reasonable for the trip may not be considered essential and could be denied as deductions.

Examples of Deductible Ordinary and Necessary Expenses:

- Airfare or train tickets for business meetings

- Hotel stays for overnight business trips

- Meals during business-related travel

2. Expenses Should Be Incurred While Traveling Away from Home Overnight for Business

A fundamental IRS rule is that travel expenses are only deductible if incurred overnight while away from your tax home.

“Tax home” is where you primarily work, not where you live. For travel expenses to qualify as tax-deductible, your trip must be far enough from this tax home that you need to sleep or rest overnight before continuing. It is not just about distance; the travel should be longer than a regular workday. This makes costs like hotel stays and meals necessary for the trip, as they are directly related to business travel and not personal commuting.

Non-Deductible Examples:

- Commuting from your home to work

- Costs incurred for personal trips mixed with business travel

3. Proper Substantiation of Expenses is Required

Proper documentation is critical to deducting travel expenses or reimbursing them tax-free. The IRS expects detailed records, typically including receipts, invoices, and logs showing the expense’s nature, amount, and business purpose. This proof is crucial in proving that the expenses were for business purposes.

At a minimum, documentation should include:

- The date and location of the trip

- The business reason for the travel

- The amount spent and supporting receipts

4. Information Should Be Collected Within 60 Days

The IRS has a time limit on when travel expenses should be documented and submitted for reimbursement to remain tax-free. Under accountable plans, employees must report and submit their expenses within 60 days of incurred costs. This timeline ensures that businesses have timely and accurate records, preventing delays that could make reimbursement taxable.

This 60-day window is critical for keeping travel expense reimbursements under an accountable plan, which allows them to remain non-taxable.

Consequences of Missing the 60-Day Deadline:

- Reimbursements are treated as income and become taxable

- They must be reported on the employee’s W-2 form

Adhering to these rules helps ensure compliance and provides a clear roadmap to keeping travel expenses tax-efficient.

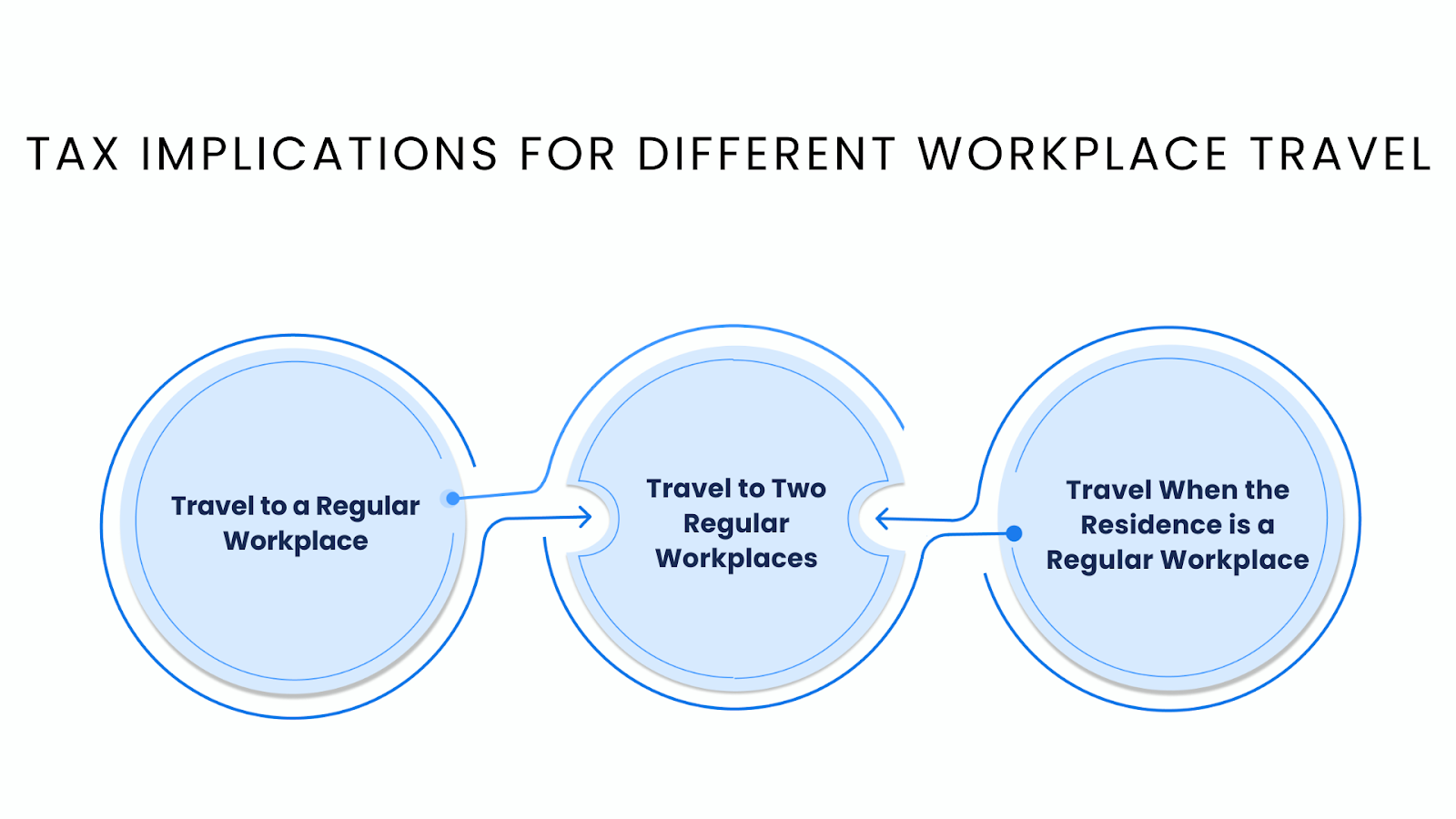

Tax Implications for Different Workplace Travel

Understanding the tax rules for different workplace travel types is crucial for employers and employees. Each situation, for example, commuting, working from home, or traveling to a temporary site, has different tax implications. Let us break it down.

1. Travel to a Regular Workplace

Commuting to your main office is considered a personal expense. The IRS views this as non-deductible, and if your employer reimburses you, it is counted as taxable income.

For example, a warehouse manager drives daily from home to the warehouse. This commuting expense is personal and not tax-deductible. If the company reimburses these commuting costs, the reimbursement is treated as taxable income, meaning the manager would have to pay taxes on that amount.

2. Travel to Two Regular Workplaces

If you work at two locations, traveling between them on the same day can be tax-free. The primary workplace is where you spend most of your time, while the secondary location is used part-time. Travel between these two workplaces is deductible as long as it’s for business.

For example, a logistics supervisor starts the day at one distribution center but travels to a second distribution hub in the afternoon. The cost of traveling between these two business locations is tax-free if both are part of the same workday for business reasons.

3. Travel When the Residence is a Regular Workplace

When your home is your primary workplace, like a home office, business-related travel from home can be tax-deductible. However, your home must meet specific IRS requirements to qualify as a legitimate business location. For example, is the space used exclusively for business, and is it the primary location where work is performed?

For example, an e-commerce business owner works from a home office, managing product listings and orders. The home is their primary workplace, meeting IRS rules (used exclusively for business). Suppose the owner travels from their home office to a third-party warehouse to inspect products. In that case, the travel expenses (such as mileage) can be tax-deductible because the home qualifies as a business location and the trip is for business purposes.

Duration-Based Scenarios for Temporary Assignments

The tax treatment of travel expenses changes based on the length of an employee’s temporary assignment. The IRS has specific rules determining when these expenses remain tax-free and become taxable.

1. Assignments of One Year or Less: Typically, Tax-Free Travel Expenses

If an employee’s assignment is expected to last one year or less, the IRS allows travel expenses to remain tax-free. This includes costs like transportation, lodging, and meals. The temporary nature of the assignment ensures that the employee’s tax home does not change, so the reimbursement stays non-taxable.

Key Examples of Tax-Free Expenses:

- Airfare or train tickets for the duration of the assignment

- Hotel stays and meal costs while away from the regular work location

- Rental cars or other necessary travel-related expenses

2. Assignments of More Than One Year or Indefinite: Tax Home Moves, Making Travel Expenses Taxable

Once an assignment is expected to last more than one year or becomes indefinite, the employee’s tax home shifts to the temporary location. When this happens, travel expenses related to the assignment are no longer tax-free.

The IRS views the new location as the employee’s main work base, so any further travel costs incurred after the move will be considered personal expenses, which are taxable if reimbursed.

Key Changes After the Tax Home Shift:

- Reimbursements for travel back to the original location become taxable.

- Lodging and meal costs at the new “temporary” location are no longer deductible.

3. Assignments Extended Beyond One Year: Tax Treatment Changes Upon Extension

If an assignment initially set for less than a year extends beyond 12 months, the tax treatment changes from that point forward. Once the one-year mark is passed, travel expenses that were previously tax-free now become taxable. This applies to all costs, as the IRS assumes the location has become a long-term or permanent work base.

Important Considerations for Extended Assignments:

- The shift from tax-free to taxable occurs when the assignment is expected to exceed one year.

- Employers and employees should monitor assignment timelines closely to avoid unexpected tax liabilities.

Special Situations in Travel Reimbursements

There are unique situations where travel reimbursements need to follow the typical rules. In such cases, the IRS treats these expenses depending on the nature and duration of the travel.

- Recurring Travel to a Temporary Workplace

If an employee occasionally travels to a temporary workplace, the IRS allows these costs to remain tax-free. For example, an employee who visits a job site or client office once or twice a month can be reimbursed without paying taxes on that money. The key here is that the travel is not regular or ongoing; it must be considered sporadic.

Key Scenarios:

- Occasional site visits for project inspections

- Rare travel to meet clients for specific work discussions

- Continuous Temporary Workplaces

An employee must have a permanent work location to be classified as itinerant. This means the employee has no set tax home. Without a tax home, all travel expenses, including lodging, transportation, and meals, are considered personal expenses and therefore taxable. This is common for employees who move frequently between temporary worksites without returning to a primary location.

What Makes an Employee Itinerant?

- No permanent work location or tax home

- Regularly moving between job sites with no fixed base

- Breaks Between Temporary Workplaces

The IRS can look at temporary assignments with breaks in between as a single extended assignment. This is called “aggregation.” If the combined total of these assignments exceeds one year, the IRS treats the employee as if they were on one long-term assignment. As a result, travel expenses that were once tax-free become taxable after the one-year mark.

What Aggregation Means for Employees?

- Temporary assignments with gaps can still be combined for tax purposes

- If the total time exceeds one year, travel expenses become taxable

Documentation and Compliance for Mileage Reimbursement

Employers often reimburse employees for using their vehicles for business travel. This covers fuel, maintenance, and wear and tear. Handling mileage reimbursement correctly ensures payments remain tax-free and follow IRS rules.

Employees must provide detailed records to keep mileage reimbursements tax-free. This includes:

- Mileage Logs: Exact miles driven for each trip.

- Dates and Destinations: When and where the travel occurred.

- Business Purpose: A clear explanation of how the travel relates to work.

Expense Reimbursement Policy Best Practices

If you do not follow the best practices for reimbursing expenses, the company and employees could face unnecessary problems. Here is what you should do to prevent these risks:

- Define Qualifying Reimbursements

Your policy should explain what counts as business-related expenses, set spending limits, and clarify allowed purchases. For example, set a daily meal limit of $50 with receipts required for approval. Limit hotel bookings or flights to specific types.

- Require Receipts

Specify which receipts are acceptable, such as register receipts or email confirmations. Also, specify how to submit them, such as scanning or using photos in software.

- Reduce Paperwork

Automate travel expense reimbursement to simplify the process, minimizing paperwork and the risk of data loss.

- Set Submission Deadlines

Establish clear deadlines to speed up the reporting process and avoid delays and missed tax opportunities.

- Create an Approval Workflow

Outline who approves expenses and what qualifies for auto-approval. Ensure managers don’t approve their reports.

- Include Audits

Define audit procedures to ensure compliance, like reviewing every third report or when expenses exceed specific amounts.

Simplifying Travel Expenses with Peakflo’s Automated Solutions

Peakflo offers an advanced travel and expense management solution that simplifies the entire process.

Key features include:

- Automated Approvals: Streamline approval processes for travel requests and expenses, saving time and reducing manual errors.

- Dynamic Expense Limits: Set customized per diem limits for employees, ensuring compliance with company policies.

- Mileage and Fuel Reimbursements: Automate the calculation and processing of mileage claims, ensuring accurate and fast reimbursements.

- Real-Time Tracking and Reporting: Gain complete visibility into travel expenses, helping with budgeting and compliance.

- Seamless Integration: Easily connects with ERPs/ accounting software, allowing smooth data transfer and improved accuracy.

Conclusion

Handling tax travel reimbursements can seem tricky, but it is easier to understand the rules and keep good records. Following IRS guidelines, tracking expenses like mileage, and knowing how temporary assignments work can help avoid tax issues.

Peakflo’s travel & expense management can simplify this, making the process faster and more accessible.

Want to see how it works in real-time? Take a demo tour today and experience the world of automation.

{kind=link}