")

Calculator Template")

: What It Is and How to Calculate")

Accurate record-keeping is crucial for effective financial management. Two key concepts that significantly ensure accurate financial records are accounts payable and accrued expenses.

Although they may seem similar, understanding the differences can help businesses manage their finances more effectively.

This article will explore the differences between accounts payable and accrued expenses.

What Are Accrued Expenses?

Accrued expenses, also referred to as accrued liabilities, are payments that a company is required to pay in the future in exchange for the goods and services received. The term “accrued” suggests an increase or accumulation, accruing expenses signify the rise of the company’s unpaid bills.

Essentially, when a company obtains a good or service, it incurs an expense and records it in its financial records, with the payment being made at a later date.

Following the accrual accounting method, expenses are acknowledged when they occur, rather than when payment is made.

Accrued expenses in the balance sheet are recorded as current liabilities and adjusted at the conclusion of each fiscal year to accommodate goods and services that have been provided but not yet invoiced.

Example of Accured Expense

An accrued expense is a cost that a business has incurred but has not yet paid. For example, let’s say a company receives consulting services in May but won’t receive the invoice until June. Although the payment hasn’t been made, the expense is recognized in May’s financial records because the service was used during that month. This practice ensures that expenses are matched with the revenues they help generate, providing a more accurate financial picture.Accrued expenses can include utilities, salaries, and interest on loans. By recording these expenses as they are incurred, businesses can maintain accurate and up-to-date financial statements, which are crucial for effective financial management and planning.

What Are Accounts Payable?

Accounts payable (AP) is the company’s ongoing, short-term expense. Usually, AP is expected to be settled within a specific period, typically 12 months from the date the expense arises. Failure to pay these expenses may result in debt repayments.

Accounts payable is a credit line provided by a supplier to a company, enabling the company to generate revenue from supplies or inventory before making payment to the supplier at a later time. This practice is prevalent among manufacturers that procure supplies or inventory from suppliers, as the suppliers grant extended payment terms

Often referred to as payables, accounts payable might not be due for 30, 60, or 90 days, and therefore, they are categorized as current liabilities. Companies document their payables on the balance sheet upon purchasing goods or services on credit. This procedure requires a double entry in the general ledger:

- A credit entry in the company’s accounts payable when the invoice is received.

- A corresponding debit entry in the expense account for the credit purchase.

Example of Accounts Payable

Tech Solutions Inc. recently purchased office supplies from Office LTD, a local supplier. On May 1st, Office LTD delivers the supplies along with an invoice totaling $5,000, due within 30 days.

The accounts payable process at Tech Solutions Inc. starts with the receiving department verifying the delivered items against the purchase order. Once confirmed, the invoice is forwarded to the finance department, where it’s reviewed for accuracy and entered into the accounting system.

The finance team schedules the payment for May 29th to take advantage of the full payment term while maintaining good cash flow management. On May 29th, Tech Solutions Inc. issues a payment to Office LTD for $5,000, recording the transaction to clear the outstanding liability from the accounts payable ledger.

By managing this process efficiently, Tech Solutions Inc. ensures timely payment to Office LTD, avoiding any late fees and maintaining a positive supplier relationship.

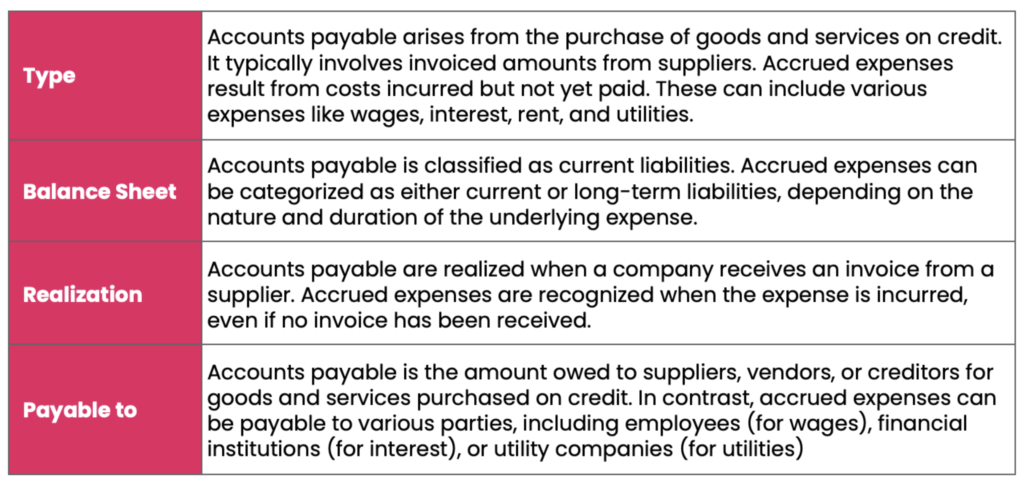

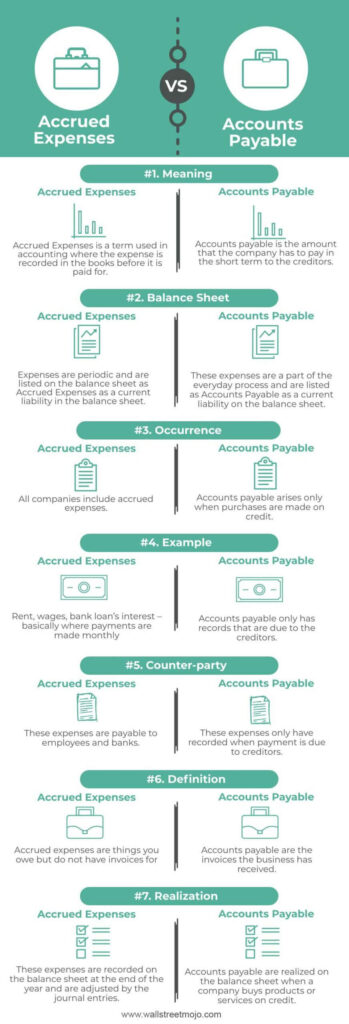

Differences Between Accounts Payable and Accrued Expenses

The distinction between accounts payable and accrued expenses is crucial for understanding a company’s financial health.

- Accrued expenses are liabilities owed for goods and services consumed but not yet invoiced, often estimated and later adjusted to the exact amount. Accounts payable, on the other hand, represents short-term debt owed to creditors for goods or services purchased on credit, with invoices already received and recorded.

- Generally, accrued expenses are related to the operating expense line item on the income statement, while accounts payable are associated with the cost of goods sold (COGS) line item.

- Accrued expenses apply to all companies and are owed to employees and banks, while accounts payable arise only when purchases are made on credit and involve payments due to creditors.

- Accrued expenses lack invoices, while accounts payable include received invoices.

- Accrued expenses are recognized on the balance sheet at the accounting year’s end via adjusting journal entries, while accounts payable are recognized when a company buys products or services on credit.

Accounts Payable vs Accrued Expense Critical Differences (Table)

Accounts Payable vs Accrued Expense Key Differences (Image)

Accounts Payable vs Accrued Expense Examples

To illustrate the differences between accrued expenses and accounts payable, let’s consider a few examples.

| Accrued Expense Examples | Accounts Payable Examples |

|---|---|

| Employee Payroll | Raw Material Purchases |

| Accrued Interest | Labor Costs |

| Monthly Building Rent | Transportation |

Example 1: Utility Expenses

A company receives its monthly utility bill on the 5th of the following month. The utility expense for the entire month is considered an accrued expense because it was incurred during the month but not yet paid. Once the company receives the utility bill, the amount owed is recorded as accounts payable, since it is now a formal obligation to pay the utility company.

Example 2: Wages

A business pays its employees bi-weekly, and the pay period ends on the 15th of the month. However, the payroll is processed, and employees are paid on the 20th of the month. The wages earned by employees from the 1st to the 15th are accrued expenses, as they have been incurred but not yet paid. On the 20th, when the payroll is processed, the accrued expense is eliminated, and the employees receive their wages.

Example 3: Interest Expense

A company takes out a loan and must pay interest on the borrowed amount. The interest is payable quarterly, but the company accrues the interest expense monthly. In this case, the interest expense is considered an accrued expense, as it is incurred monthly but not yet paid. At the end of the quarter, when the interest payment is due, the company records the amount as accounts payable, since it now has a formal obligation to pay the financial institution.

Make Your Accounts Payable Management Easier

In conclusion, while both accrued expenses and accounts payable are liabilities that a business incurs, there are some key differences between the two. Accrued expenses refer to expenses that have been incurred but not yet paid, while accounts payable are amounts owed to vendors or suppliers for goods or services that have already been received but not yet paid for.

To manage these liabilities efficiently, businesses can turn to automation solutions like Peakflo. With end-to-end AP automation, Peakflo can centralize and streamline procurement to payment processes, making vendor payment processes more efficient and budgeting more accurate and simple to analyze.

As Poetri, a Senior Finance and Tax Manager at Rey, can attest, Peakflo’s support team is approachable, supportive, and constantly updating the platform with new features to support business transactions.

If you’re looking to improve your AP processes and streamline your payments, consider giving Peakflo a try.

FAQ

1. Are accrued expenses the same as accounts receivable?

No, accrued expenses and accounts receivable are different. Accrued expenses are current liabilities on your balance sheet, representing amounts owed to vendors, suppliers, or other creditors. Accounts receivable, on the other hand, is an asset on your balance sheet, representing money owed to you by your customers.

2. How does an accrued expense differ from an expense?

An expense is a general term for costs a business incurs during regular operations. An accrued expense is a specific type of expense recorded in your general ledger to ensure accuracy. While expenses can be fixed, variable, or periodic, accrued expenses specifically need to be recorded for a specific accounting period.

3. When should you accrue an expense?

Accruals should be made as part of financial close management at the end of the accounting period. This ensures financial statements are accurate. For example, if you haven’t received a utility bill by the end of the month, you estimate and accrue the utility expense. Once the actual bill is received, you reverse the accrual and enter the actual amount into accounts payable.

4. How are accrued expenses recorded?

Accrued expenses are recorded by making an adjusting journal entry at the end of the accounting period. For example, if commissions totaling $3,500 are owed for sales made in March but will be paid in April, you would debit the Commission Expense account and credit the Accrued Expenses account. This ensures the expense is recognized in the correct period. Once the payment is made, you reverse the accrual and record the payment through accounts payable.

5. Is accrued income an asset?

Yes, accrued income is considered an asset on the balance sheet. It represents revenue that has been earned but not yet received in cash. This income is recorded as an asset because it is expected to be received in the future, reflecting the company’s right to collect money for goods or services already provided.

{kind=link}