")

Calculator Template")

: What It Is and How to Calculate")

Cash flow problems don’t knock—they barge in. Grow your business with proactive and reliable cash flow management strategies.

Are you constantly chasing down payments, unsure of when your cash will hit the account? Or maybe your company’s growth is being held back by rising expenses and unpredictable revenue cycles? If these sound familiar, you’re not alone.

Effective company cash flow management is not just about paying bills and collecting invoices—it’s about having a strategic system that ensures your business can survive and thrive.

What is Cash Flow Management?

Of the 400,000 businesses that open yearly, half close within five years due to poor cash flow management. 82% of failed companies point to cash flow issues as a primary cause. Effective cash flow management involves overseeing the movement of funds in and out of your business and using that data to create budgets and forecasts. This provides a clear financial roadmap and the flexibility to pay off debts, invest in opportunities, and maintain reserves.

Positive cash flow means bringing in more than you’re spending, enabling growth. Negative cash flow signals overspending, leading to cash shortages, rising debt, or needing external funding. The goal is to strike the right balance—having enough cash to meet obligations while preventing excess cash from sitting idle.

Tracking and Controlling Money Flow

Tracking and controlling your money flow is the foundation of business cash flow management. It involves monitoring every financial transaction—knowing exactly when cash comes in and where it goes out. By tracking income and expenses, businesses can prevent cash shortages, leading to missed opportunities and financial instability, and avoid overspending, which can strain your resources and hinder growth. This visibility helps you stay in control of your finances, ensuring that your business runs smoothly and efficiently.

Example: A logistics company dealing with high shipping costs should regularly review cash flow reports to ensure they’re not overspending on operations. With an automated payment system, you can avoid manual errors and speed up payment processing, giving you greater control over cash flow.

Key tactics for tracking and controlling cash flow:

- Automate payment tracking to monitor incoming and outgoing payments in real time.

- Conduct regular cash flow reviews to spot unusual trends or discrepancies.

- Set alerts to notify you of low cash reserves before they become critical.

Forecasting Cash Flow Needs

Good company cash flow management means tracking cash and forecasting future needs. Forecasting lets you predict when cash will be available and when you might face shortfalls. Without this foresight, businesses risk running out of cash at critical times, leading to missed opportunities, delayed payments, or even business closure. Businesses can anticipate challenges using historical data and current trends, ensuring they have the cash necessary for upcoming expenses, payroll, or investments.

For instance, an e-commerce business can forecast cash flow to plan for high-demand periods like Black Friday. This allows them to allocate funds for inventory and marketing well in advance, ensuring they won’t run out of stock or lose sales due to cash shortages.

Best practices for forecasting cash flow:

- Use automated forecasting tools to create monthly or quarterly cash flow projections.

- Plan for seasonal fluctuations by analyzing past trends.

- Forecasts should be updated often to account for shifting market conditions.

Managing Finances for Business Growth

Effective company cash flow management is not just about day-to-day survival—it’s about setting the stage for growth. When properly managed cash, businesses can reinvest in opportunities, expand operations, or develop new products. Automated cash flow and cash management enable you to seize growth opportunities without risking your financial health.

Example: A growing marketplace business, for example, might use cash flow management to scale its infrastructure, hire additional staff, or expand into new markets. By managing cash carefully and automating collections, businesses can secure the funds needed for growth without stressing about cash shortages.

Strategies for managing cash flow for growth:

- Reinvest a portion of profits to fund expansion or new projects.

- Automate invoice collection to speed up receivables and free up cash.

- Establish a business line of credit to support growth during lean periods.

Now that we understand its role let’s examine why mastering cash flow management is crucial for business success.

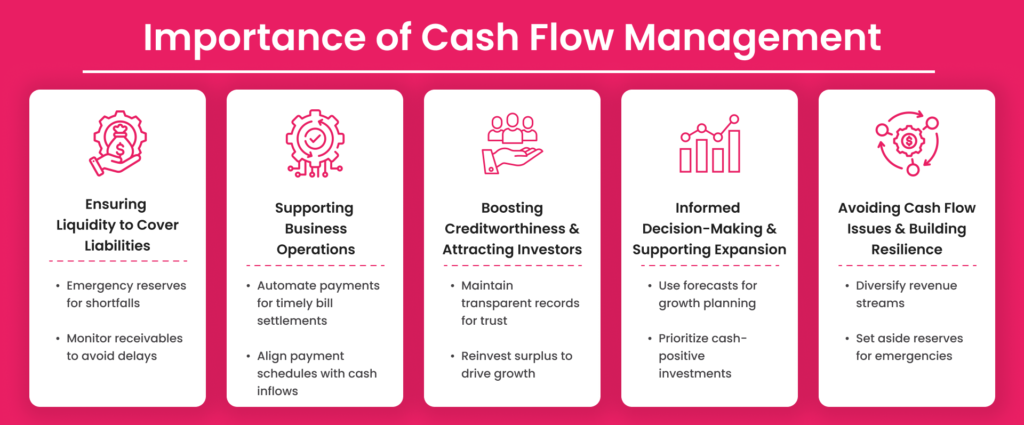

The Importance of Cash Flow Management

The cash flow management market was valued at $727.3 million in 2023, and it’s on track to skyrocket to $6.17 billion by 2032. With a projected annual growth rate of 26.82% from 2024 to 2032, this market is set for impressive expansion over the coming years.

Let’s explore why managing your cash flow is crucial and how it can drive business success.

Ensuring Liquidity to Cover Liabilities

Without enough cash, businesses risk missing payroll or defaulting on supplier payments. This can lead to service disruptions and damaged relationships. Small retail enterprises may prevent shortages during seasonal downturns by cash flow monitoring, utilizing cash buffers, and negotiating longer payment terms with suppliers.

Supporting Business Operations

A business with consistent cash inflow can cover expenses like rent, salaries, and utilities without interruption. For example, a logistics company may rely on predictable cash flow to maintain its fleet, ensuring deliveries are not delayed due to cash shortages.

Boosting Creditworthiness and Attracting Investors

Investors and lenders look for businesses that have stable cash flow. If your company consistently manages its cash well, it increases your creditworthiness and makes it easier to secure loans or investments. A startup that showcases positive cash flow projections is far more likely to attract investors willing to fund its growth.

Informing Decision-Making and Supporting Expansion

Proper company cash flow management gives you the data you need to make smart business decisions. For example, an e-commerce company might use cash flow data to prepare a new marketing campaign without risking its core operations.

Avoiding Cash Flow Issues and Building Resilience

Cash flow mismanagement can lead to financial crises. But businesses that stay on top of their cash can build resilience, allowing them to weather downturns or unexpected expenses. During the pandemic, businesses with strong cash reserves could maintain operations and adapt to market changes.

With the importance of cash flow management in mind, let’s look at the key components that help maintain financial stability and drive optimization.

Components of Cash Flow Management

Effective company cash flow management requires closely monitoring several key areas. Let’s break down the essential components that make or break your business’s cash flow—and explore how you can optimize them to avoid common pain points.

Accounts Payable

Struggling to pay vendors on time? Or worse, juggling payments to avoid late fees? That’s where accounts payable come in. Managing your outgoing payments effectively can prevent cash flow shortfalls and keep supplier relationships intact. If you’re not on top of this, you might end up paying bills before your clients have paid you, leaving you in a financial bind.

Examples: For example, a $500 office supply invoice logs as a $500 credit in payables. The expense shows up on the income statement even though the payment hasn’t been made yet—that’s how accrual accounting works.

Once the bill is paid, $500 is credited to the cash account, and accounts payable gets debited.

If the company also gets a $50 invoice for lawn care, the total in accounts payable would be $550 until both are paid.

What can you do?

- Negotiate better payment terms to align with when cash comes in.

- Automate payments to avoid delays and late fees, freeing time and reducing manual errors.

| Aspect | Meaning |

| Definition | Money a business owes to suppliers or vendors |

| Type of Account | Liability |

| Impact on Cash Flow | Decreases cash when payments are made |

| Where It Appears | Liability section of the balance sheet |

| Payment Status | Represents unpaid bills that will eventually be paid |

Accounts Receivable

Are your customers dragging their feet when it’s time to pay? Accounts receivable are often the root of cash flow issues for many businesses. The longer it takes to collect payments, the tighter your cash reserves get. Late receivables leave you scrambling to cover expenses.

Example: Similar to the previous example, when a business sends a $500 invoice to a client for services, they record it as a $500 debit in accounts receivable and a $500 credit to revenue. Even though the cash hasn’t been received yet, the revenue is recognized immediately—this follows accrual accounting.

Client payment credits $500 to receivables and debits cash.

If the business also invoices another client $50 for additional services, the total in accounts receivable would be $550 until both payments are collected.

How to fix it?

- Set up automated invoice reminders to encourage on-time payments.

- Offer discounts for early payments and enforce penalties for late ones to keep the cash flowing.

| Aspect | Meaning |

| Definition | Money owed to a business by customers |

| Type of Account | Asset |

| Impact on Cash Flow | Increases cash when payments are received |

| Where It Appears | Asset section of the balance sheet |

| Payment Status | Represents sales that will eventually be collected |

Inventory Management

Is your money tied up in unsold inventory? This is a common company cash flow management problem for businesses that hold too much stock. Inventory management is about finding that spot between having enough products to meet demand without overinvesting in stock that sits on your shelves, eating into your cash flow.

Example: Let’s say you own a clothing store and order $10,000 worth of inventory. Half sells in the first month, leaving $5,000 of unsold stock. While it sits on your shelves, your cash is tied up, limiting other investments like marketing or new products.

Good inventory management helps avoid this by ordering just enough to meet demand, keeping your cash flow healthy. If you’d only ordered $6,000, you’d have more flexibility for other needs.

How to get it right?

- Use data to forecast demand accurately and avoid over-ordering.

- Turn to just-in-time inventory strategies to keep stock levels lean and cash flow healthy.

As we’ve seen, managing various components is crucial to maintaining a healthy cash flow. One key area that ties it all together is accounts payable (AP) and its direct impact on cash flow management.

The Relationship Between AP and Cash Flow Management

Accounts payable (AP) plays a vital role in maintaining healthy cash flow management, as it represents the funds owed to vendors. Effective AP management requires balancing timely payments and strategic delays to preserve cash reserves without straining supplier relationships. Delaying payments can free up cash but risks late fees and damaged credit, while paying too quickly can deplete resources needed elsewhere.

To optimize this balance, businesses can negotiate favorable payment terms or automate invoice processing for better accuracy and timeliness. AP automation also improves cash flow forecasting, ensuring smoother payment cycles and financial stability.

By leveraging these strategies, companies can manage their cash flow more efficiently, prevent unnecessary costs, and maintain strong supplier partnerships, contributing to long-term operational success.

Understanding the role of AP within the broader cash flow strategy ensures businesses avoid cash shortages while maximizing their ability to invest in growth and manage their financial obligations.

Types of Cash Flow

Cash flow is not just about what’s coming in and going out—it’s about where that money is coming from and where it’s headed. Understanding the different types of cash flow helps you see exactly how your business is performing. Let’s dive into the three key types of cash flow that every business needs to keep an eye on.

Cash Flows from Operations (CFO)

Are your daily operations draining cash faster than they’re bringing it in? Cash flow from operations (CFO) reflects the money your core business activities generate—sales, services, and everyday expenses. If your operations are not cash-positive, you could be in trouble, even if your sales look good on paper.

There are two ways to calculate this:

Indirect Method:

- Cash Flows from Operations = Net Income + Non-Cash Expenses – Increase in Working Capital

Direct Method:

- Cash Flows from Operations = Cash Receipts from Customers – Cash Payments to Suppliers and Employees – Interest Paid – Income Taxes Paid

Example:

Let’s calculate Cash Flows from Operations for a company with the Indirect method:

- Net Income: $100,000

- Depreciation: $20,000

- Increase in Accounts Receivable: $10,000

- Increase in Inventory: $5,000

- Increase in Accounts Payable: $7,000

Using the indirect method formula:

Cash Flows from Operations = $100,000 + $20,000 – $10,000 – $5,000 + $7,000

= $112,000

What can you do?

- Regularly review cash flow statements to ensure operations are generating enough cash.

- Streamline expenses and boost revenue to keep some money moving in the right direction.

Cash Flows from Investing (CFI)

Is your business making the right investments, or is your money tied up in unused assets? Cash flow from investing (CFI) includes the cash spent or gained from long-term assets like equipment, property, or investments. A negative CFI can signal that a company is investing in growth, but it’s a red flag if it’s consistently in the red without returns.

The formula for calculating cash flows from investing activities (CFI) is:

- CFI = Capital Expenditures + Purchase of Long-Term Investments + Business Acquisitions – Divestitures

Example:

Let’s say a company has the following investing activities for the year:

- Purchased $20 million in PP&E (CapEx)

- Bought $5 million in marketable securities

- Acquired a business for $10 million

- Sold off an investment for $3 million

Plugging these values into the formula: CFI = -$20 million – $5 million – $10 million + $3 million = -$32 million

How to manage it?

- Carefully evaluate the return on investments before purchasing expensive assets.

- Make sure your operational cash flow can support investment spending.

Cash Flows from Financing (CFF)

Are you relying too much on external financing? Cash flow from financing (CFF) tracks the money your business receives or spends from borrowing or repaying loans, issuing stock, or paying dividends. Relying on loans can drain future cash flow with interest.

To calculate cash flows from financing activities (CFF), you can use the following formula:

- CFF = Cash Inflows from Issuing Equity or Debt – (Dividends Paid + Repurchase of Debt and Equity)

Example:

Let’s consider a company with the following financing activities for the year:

- Cash inflows from issuing new equity: $200,000

- Cash inflows from issuing new debt: $300,000

- Dividends paid: $50,000

- Repurchase of equity: $100,000

Using the formula:

Calculate total cash inflows:

- Total Cash Inflows = Cash Inflows from Issuing Equity + Cash Inflows from Issuing Debt

- Total Cash Inflows = $200,000 + $300,000 = $500,000

Calculate total cash outflows:

- Total Cash Outflows = Dividends Paid + Repurchase of Equity

- Total Cash Outflows = $50,000 + $100,000 = $150,000

Now, calculate CFF:

- CFF = Total Cash Inflows – Total Cash Outflows

- CFF = $500,000 – $150,000 = $350,000

Best practices:

- Balance external financing with cash generated from operations to avoid over-reliance on debt.

- Plan loan repayments carefully to prevent cash flow bottlenecks.

| Aspect | Cash Flows from Operations (CFO) | Cash Flows from Investing (CFI) | Cash Flows from Financing (CFF) |

Outline | Cash generated or used from a company’s core business activities, such as sales and expenses. | Cash is used for or generated by investments in long-term assets like property, equipment, or securities. | Cash from issuing or repaying debt, equity, or paying dividends to shareholders |

| Impact on Business | Reflects the company’s ability to generate cash through normal operations | Reflects how much cash is being invested in long-term growth or divested from assets | Reflects cash changes related to financing, such as raising or repaying capital |

| Example | A company sells $100,000 of products, collects $80,000 in cash, and pays $50,000 in operating expenses. CFO is $30,000. | The company spends $50,000 to buy new equipment and receives $10,000 from selling old machinery. CFI is -$40,000. | The company raises $100,000 and pays $20,000 in dividends. CFF is $80,000. |

| Positive Cash Flow Meaning | Indicates strong operational performance, and the company can cover expenses from its core activities | Suggests the company is investing in future growth or receiving returns from investments | Reflects capital being raised to fund operations or investments or repayment of financing obligations |

| Negative Cash Flow Meaning | This could indicate trouble covering day-to-day expenses if persistent | Indicates heavy investment or asset sales, which could be either a sign of growth or downsizing | Shows repayment of debts or returns to shareholders or insufficient financing inflows |

Despite your best efforts, cash flow challenges can still arise—here’s a look at the most common issues and how to navigate them

Common Cash Flow Management Issues

Company cash flow management can be tricky, especially when certain business challenges throw you off course. Let’s explore some of the most common issues businesses face—and how to navigate them.

Cycling Industries

Does your business experience regular ups and downs? In industries like construction or agriculture, cash flow tends to cycle with the seasons, making it tough to maintain steady operations year-round. When the off-season hits, you might struggle to cover operating costs, leading to cash shortages.

| Example | Solution |

| Construction companies often face cash flow issues during winter when projects slow down. They can combat this by building a cash reserve during busier months to stay afloat during the slower periods. | Forecast your cash flow based on industry cycles and set aside a reserve fund for slower periods. |

Variable Patterns of Revenue

Does your business income fluctuate wildly from month to month? If so, managing cash flow can feel like a rollercoaster. One month, you might be flush with cash, while the next, you struggle to cover basic expenses. Businesses like consulting firms or event-based services often see this issue.

| Example | Solution |

| A wedding planning business has high revenue during peak season, but cash dries up in the off-season. To manage, they may spread their expenses out by negotiating longer payment terms with vendors. | Use cash flow forecasts to predict lean months and manage expenses carefully during high revenue periods. |

Rapid Expansion

Are you growing so fast that you can’t keep up financially? Rapid expansion sounds like a dream come true, but it often leads to cash flow problems if your expenses outpace your incoming cash. You might be hiring new staff, investing in equipment, or expanding your location, all of which eat into your cash reserves.

| Example | Solution |

| A tech startup growing its team and infrastructure was short cash for day-to-day operations. They can take out a line of credit to cover expansion costs while waiting for revenue growth to catch up. | Balance your growth ambitions with cash flow management by pacing investments and securing flexible financing options. |

Lack of Accounts Receivable System

A poor accounts receivable system can leave your business struggling for cash, even if your sales are strong. Late or missed customer payments mean less money available for your bills. Additionally, chasing payments takes up valuable time and resources without a streamlined system.

| Example | Solution |

| A small B2B supplier struggled with late client payments, affecting their ability to pay vendors. They can speed up their collections process by implementing an automated invoicing system with reminders. | Implement an automated accounts receivable system to send timely invoices and reminders, reducing payment delays. |

Extending Credit

Are you offering credit to customers who are struggling to get paid back? Extending credit can boost sales and tie up your cash in unpaid invoices. If you’re careless, this can leave you without enough money to pay your bills.

| Example | Solution |

| A furniture store offered flexible payment terms to customers, which boosted sales but created a cash flow gap. They can solve this by tightening their credit terms and offering early payment incentives. | Establish strict credit policies and offer discounts for early payments to keep cash flowing. |

Projecting Expenses

Are your expense projections consistently off? Underestimating your costs can create serious cash flow problems when unexpected expenses arise. You might be scrambling to cover bills if you’re not accurately forecasting your outlays.

| Example | Solution |

| An e-commerce business underestimated shipping costs during a sales surge, leading to a shortfall. They can adjust this by building more detailed expense projections based on sales patterns and historical data. | Create detailed and realistic expense projections, including room for unexpected costs, to avoid cash shortages. |

Having pinpointed the challenges, we can now focus on strategic approaches to enhance your cash flow management efforts.

Effective Cash Flow Management Strategies

Cash flow issues don’t have to be a constant business breaker. You can turn things around with the right strategies and keep your business running smoothly. Let’s look at some proven cash flow management techniques.

Invoice Promptly and Follow-Up

One of the simplest ways to improve cash flow is to send invoices as soon as the job is done. Don’t wait weeks to bill your customers; be proactive with follow-ups if late payments are made.

- Quick Fix: Set up an automated invoicing system that sends reminders and ensures no invoice slips through the cracks. This helps you get paid faster and keeps your cash flowing.

Optimize Inventory Management

If you’re holding too much inventory, it’s like having money locked away that could be better used elsewhere. Finding the balance between meeting customer demand and not overstocking is key.

- Easy Solution: Use data to forecast demand and keep inventory levels lean. A just-in-time inventory approach can free up cash for other areas of your business.

Extend Payables (the Right Way)

Need a little breathing room? Stretching out your payables without damaging relationships can give you more time to manage your cash flow. The trick is to negotiate terms that work for you and your suppliers.

- Pro Tip: Build good relationships with your vendors and negotiate extended payment terms without hurting trust. This gives you more time to collect your payments and keep cash in your account longer.

Find Flexible Financing Options

Running low on cash but don’t want to take on too much debt? Flexible financing can offer a lifeline when you need a boost, but you must be smart about it. Whether it’s a line of credit or invoice factoring, choose options that won’t bury you in interest payments.

- Smart Move: Explore short-term financing solutions like invoice factoring or a business line of credit. These options give you access to cash when needed without the long-term burden of loans.

Use Technology for Cash Flow Forecasting

Are you guessing when it comes to your future cash flow? Technology can take the guesswork out of managing your finances. Cash flow forecasting tools help you predict when cash will come in and go out, allowing you to plan and avoid surprises.

- Tech Tip: Use a cash flow forecasting tool that integrates with your accounting software. This gives you real-time insights and helps you spot potential shortfalls before they happen.

Opt for Cost-Effective Tools

Think managing cash flow is expensive? It doesn’t have to be. Plenty of affordable tools can help you manage payments, track invoices, and forecast cash flow—all without breaking the bank.

- Budget-Friendly Tip: Peakflo AI provides affordable tools to streamline payments and invoicing, reducing manual work and errors while saving costs—all in one powerful solution.

Examples of Cash Flow Management

Real-world examples often illustrate the power of effective cash flow management—let’s examine how these businesses turned their challenges into successes.

Example A – Short on Cash: Managing Receivables, Payables, and Inventory

Driver Logistics improved their cash flow by reducing their average overdue days by 16 and increasing receivable efficiency by 35% using Peakflo. By optimizing how they collected payments and managed receivables, they freed up cash to cover operational expenses without relying on external funding.

Example B – Extra Cash: Opportunities for Investment and Growth

InMobi used Peakflo to increase invoicing efficiency by 100% and decrease overdue by 9 days. This improvement gave them extra cash to invest in scaling their operations and expanding their services.

These case studies show how businesses can manage cash flow challenges and use extra cash to fuel growth.

How Peakflo Helps Businesses Manage Cash Flow

Peakflo offers comprehensive solutions to streamline cash flow management, addressing common pain points like delayed payments, inefficient billing processes, and poor financial visibility. With Peakflo’s automated accounts receivable (AR) and accounts payable (AP) features, businesses can:

- Accelerate Collections: Automated reminders for overdue invoices reduce the time businesses wait for payments, improving cash inflow predictability.

- Streamline Bill Payments: AP automation reduces errors, ensuring vendors are paid on time and avoiding late fees and disruptions in supply chains. This enables businesses to manage outflows more effectively.

- Real-Time Cash Flow Tracking: Peakflo provides AI-powered cash flow tracking and forecasting in real-time into both AR and AP, offering better visibility into the company’s current financial status. Businesses can forecast future cash flow more accurately.

- Custom Approval Workflows: By setting automated, custom workflows for invoice approvals, Peakflo helps reduce bottlenecks in payment processing, ensuring faster approval cycles. This leads to more efficient handling of outgoing payments.

- Centralized Communication: Peakflo’s platform consolidates all financial communication in one place, ensuring that payment schedules and invoice details are accessible to both internal teams and external vendors. This reduces misunderstandings and speeds up cash flow processes.

These tools empower businesses to reduce manual workloads, enhance liquidity, and maintain smooth operations by ensuring timely payments and collections, ultimately strengthening their financial health.

Conclusion

Any successful company is built on strong cash flow management. By managing receivables, payables, and expenses efficiently, companies can avoid cash shortages and capitalize on growth opportunities. Implementing effective strategies and using the right tools ensures a consistent cash flow, allowing businesses to thrive.

Peakflo is your go-to solution for automating cash flow processes, helping you avoid cash issues while reducing manual work and errors.

Ready to take control of your cash flow? Request a demo and see Peakflo in action today!

{kind=link}