")

Calculator Template")

: What It Is and How to Calculate")

Payment delays can create serious problems for businesses. When a transaction doesn’t go through on time, vendors start following up, cash flow slows down, and finance teams rush to fix errors. Unclear payment processes make things worse, leading to extra fees, compliance risks, and strained vendor relationships.

A structured payment process helps businesses avoid these issues. It ensures that payments are processed on time, reduces mistakes, and keeps financial records accurate. Businesses with an efficient payment system can speed up transactions, lower costs, and avoid last-minute reconciliations.

In this blog, we’ll explain how the payment process works, why it matters, and how businesses can improve it. Whether you collect payments from customers or pay vendors, a smooth system helps keep cash flow steady and financial operations running without disruptions.

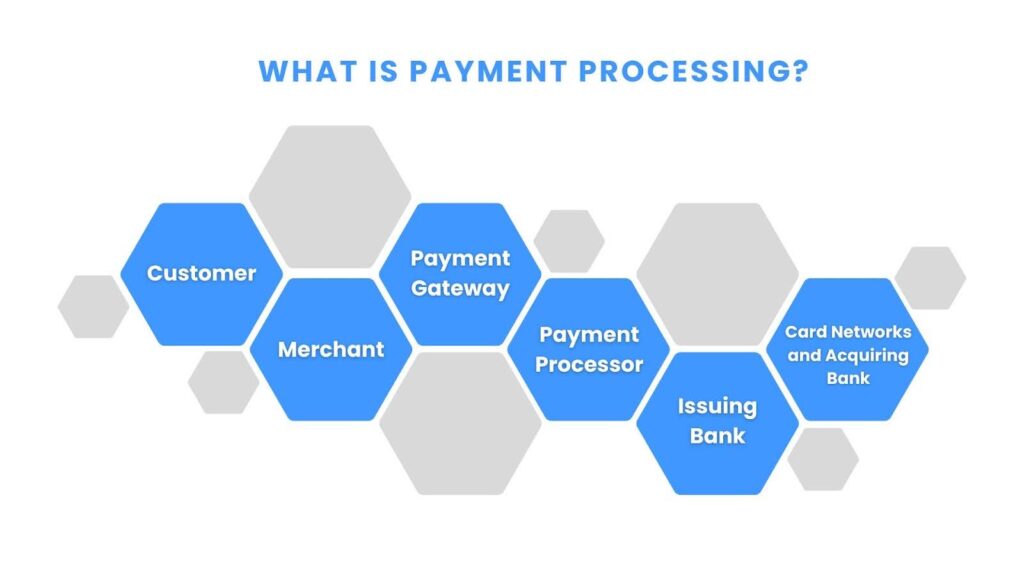

What is Payment Processing?

Payment processing is how businesses receive money from customers after a purchase. It makes sure transactions are quick, secure, and accurate. A smooth payment system helps businesses manage cash flow while giving customers a hassle-free way to pay.

Every transaction follows a set process to keep payments safe and reliable. Here’s how it works:

When customers buy something online, they enter their payment details at checkout. The payment processor then sends this information to the bank that issued the customer’s card. The bank checks whether the payment is valid and approves or declines it. If approved, the money is transferred to the business’s merchant account.

This process happens in seconds, allowing businesses to collect payments without delays or security risks.

Learning how payment processing works doesn’t solve the problem of payment delays. Many other factors can cause delays in this workflow. Knowing the workflow is important to understanding the cause of delays.

Key Components and Workflow of Payment Processing

Understanding payment processing starts with knowing its key components and steps. Each part plays an essential role in ensuring smooth and secure transactions. Here’s how these components connect in the workflow:

1. Customer

The process starts with the customer, who provides accurate payment details such as their card numbers or bank account information while making a payment. Data accuracy helps the transaction to proceed smoothly.

Example: A customer shopping online enters their card details at checkout to complete the purchase.

2. Merchant

Next is the merchant, the business that receives the payment. The merchant collects payment details while keeping track of their sales and balancing financial records. A smooth process helps avoid errors and allows your business to run without interruptions.

Example: A clothing store receives payments through its e-commerce platform and uses the information to update its sales records.

3. Payment Gateway

The payment gateway acts as a secure bridge. It encrypts customer data before sending it to the processor.

Example: During an online purchase, the gateway prevents fraud by ensuring the buyer’s credit card details are securely transmitted.

4. Payment Processor

The payment processor handles the technical side of the transaction. It communicates with the issuing bank to verify that funds are available. If all checks are clear, it authorizes the transaction, reducing errors and delays.

Example: When a customer pays for groceries at the store, the payment processor quickly checks with the customer’s bank to confirm if the payment can go through.

5. Issuing Bank

The issuing bank reviews the customer’s account to confirm there are enough funds or credit. Once approved, it sends a confirmation back through secure channels to the payment processor.

Example: A bank that issues customers a credit card checks the balance of their account before approving a payment at a restaurant.

6. Card Networks and Acquiring Bank

Card networks like Visa and Mastercard connect the issuing bank with the acquiring bank, which holds the merchant’s account. Once the transaction is approved, the acquiring bank deposits the funds into the merchant’s account, completing the process.

Example: After a customer pays for groceries with a Visa card, the card network communicates with the acquiring bank to deposit the funds into the supermarket’s account.

These components work together to create a seamless flow from the customer to the merchant. Now, we will explore the different payment methods available.

Types of Payment Methods

Customers expect fast and secure ways to pay. If a business only offers limited payment options, it risks losing sales. Some customers prefer credit cards, while others use digital wallets or bank transfers. When businesses accept multiple payment methods, they reduce checkout frustrations, improve cash flow, and create a better experience.

Here are the most common payment methods and how they impact businesses:

1. Credit and Debit Cards

Cards are one of the most common ways people pay. They allow quick transactions both online and in stores. Accepting card payments means faster checkouts and fewer abandoned sales. Businesses that don’t offer card payments may struggle to attract customers who prefer cashless options.

2. Digital Wallets

More people are using Apple Pay, Google Pay, and PayPal for everyday purchases. Instead of entering card details, they can tap or click to complete a payment. This makes the checkout process faster and easier, reducing cart abandonment. Businesses that accept digital wallets create a smoother buying experience and increase conversions.

3. Bank Transfers

Bank transfers are often used for large payments and business-to-business transactions. They provide a secure and reliable way to transfer money directly between accounts. Some businesses prefer them because they avoid credit card processing fees. However, they take longer to process, which can slow down cash flow.

4. Cryptocurrencies

Some businesses accept Bitcoin and other cryptocurrencies. These transactions are secured through blockchain technology, making them safe from fraud. While not widely used yet, accepting cryptocurrency can attract tech-savvy customers and global buyers. However, price fluctuations and limited adoption make it less practical for everyday sales.

Comparison of Payment Methods

Each payment method has advantages, but the right choice depends on your business model and customer preferences. If you run an e-commerce store, offering credit cards and digital wallets can reduce abandoned carts and speed up checkouts. If your business handles large transactions, bank transfers provide a secure way to move funds. While cryptocurrency payments are still uncommon, they can attract tech-savvy customers looking for alternative payment options.

| Payment Method | Speed | Security | Convenience |

| Credit/Debit Cards | Instant | High | High |

| Digital Wallets | Instant | Very High | Very High |

| Bank Transfers | 1-3 Business Days | High | Moderate |

| Cryptocurrencies | Varies | Very High | Moderate |

But payment processing is more than just offering different methods. It’s also about making sure payments are fast, reliable, and fraud-proof.

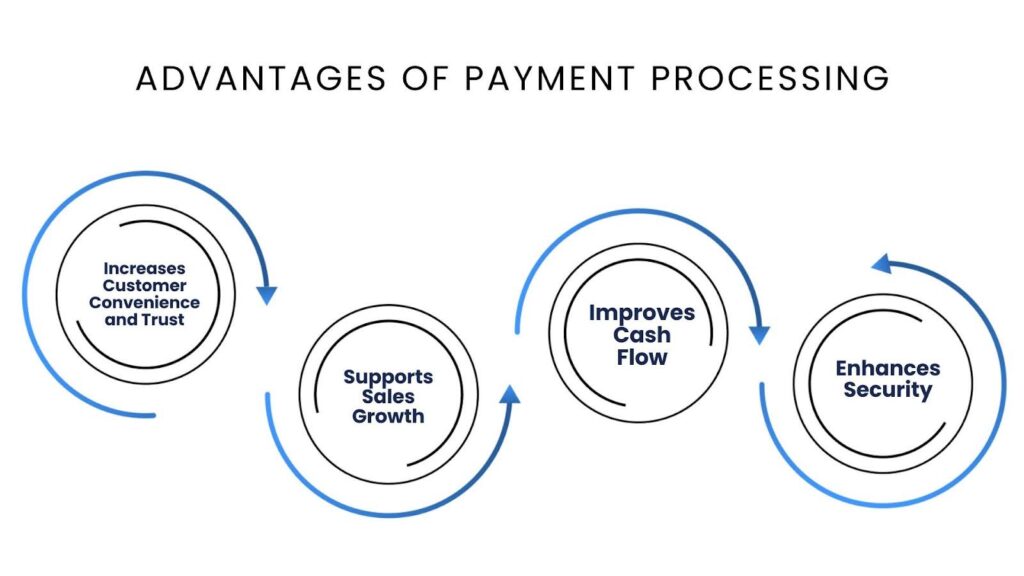

Advantages of Payment Processing

Managing payments can be frustrating when transactions fail, take too long, or come with high fees. Customers expect fast and secure payment options, and businesses need a system that keeps cash flow steady. When payments are delayed or rejected, it creates unnecessary stress for both sides. A structured payment process helps businesses process transactions on time, reduce errors, and protect against fraud. Here’s why it matters:

1. Faster and Safer Transactions

Customers want a smooth and secure way to pay. Whether using credit cards, digital wallets, or bank transfers, they expect payments to go through without problems. A reliable payment system helps businesses provide a seamless experience, reducing abandoned transactions and customer complaints.

2. More Payment Options, More Sales

Not everyone pays the same way. Some customers prefer digital wallets, while others use online banking or credit cards. Businesses that accept multiple payment methods can reach more customers, reduce cart abandonment, and increase revenue.

3. Stronger Cash Flow Control

Late payments can disrupt business operations. A structured payment process ensures that businesses get paid on time, making it easier to cover expenses, pay vendors, and plan for growth. Faster settlements also reduce the need for constant follow-ups on unpaid invoices.

4. Better Security and Fraud Prevention

Fraud is a major risk in payment processing. Modern payment systems use encryption and fraud detection tools to keep transactions safe and protect customer data. This reduces chargebacks, financial losses, and compliance risks.

These advantages support business growth, improve customer satisfaction, and increase operational efficiency. Next, we will examine the security measures that protect payment systems and keep them reliable.

Security in Payment Processing

As more payments happen online, keeping transactions safe is more important than ever. A security breach can expose customer data, cause fraud, and hurt a business’s reputation. If customers don’t feel safe making payments, they may take their business elsewhere.

To prevent this, businesses use security measures to protect transactions and customer data. Here’s how they do it:

1. Encryption: Protecting Payment Data

Encryption scrambles payment details into unreadable code before sending them across networks, preventing hackers from stealing sensitive information.

For example, when customers enter their credit card details, encryption ensures that only the payment processor can read the information. Even if someone intercepts the data, they won’t be able to use it.

2. Tokenization: Replacing Card Details with Secure Tokens

Tokenization replaces payment details with a unique token that has no real value. This means businesses don’t have to store actual card numbers, reducing the risk of data theft.

Many businesses use tokenization to secure saved payment details for returning customers. Digital wallets like Apple Pay and Google Pay use this method to keep payments safe.

3. Authentication: Verifying Customer Identity

Fraudsters often try to use stolen card details to make payments. Authentication tools help confirm that the person making the payment is the actual cardholder.

Some common authentication methods include:

- Multi-Factor Authentication (MFA): Requires a password and a one-time code sent to a phone or email.

- Biometric Verification: Uses fingerprint scanning or facial recognition to confirm identity.

- One-Time Passwords (OTP): Sends a unique code to complete the transaction securely.

These steps help prevent fraud and unauthorized payments, especially for large transactions.

4. Compliance: Following Security Rules

Businesses that accept card payments must follow strict security standards, the most important of which is PCI DSS (Payment Card Industry Data Security Standard). These rules ensure that businesses handle payment data safely.

Following these security standards helps businesses:

- Prevent fraud and data breaches.

- Avoid legal penalties for not securing payments.

- Build customer trust by keeping transactions safe.

Ignoring these rules can lead to data theft, heavy fines, and lost customers.

A secure payment process protects both businesses and customers. It reduces fraud, prevents chargebacks, and ensures payments are processed safely. When security is in place, businesses can focus on speeding up transactions, improving cash flow, and creating a better customer experience.

Secure transactions allow businesses to build trust with their customers, and improving the payment process helps increase customer satisfaction. Let’s examine the best practices for improving customer experience.

Payment Processing Best Practices

A smooth payment process keeps cash flow steady and makes payments easier for businesses and customers. When payments fail or take too long, it can cause delays, security risks, and lost sales. Here are some simple steps to improve payment processing and avoid common problems:

1. Pick a Reliable Payment Processor

Not all payment processors work the same way. A good provider should offer fast transactions, strong security, and reliable support. It should also connect easily with your accounting and invoicing systems to keep payments organized.

2. Offer Payment Options That Customers Use

Some customers prefer credit cards, while others use digital wallets or bank transfers. Giving them choices makes it easier to complete purchases. It also reduces abandoned checkouts and helps businesses increase sales.

3. Use Fraud Protection Tools

Fraud can lead to chargebacks, financial losses, and security risks. Many modern payment systems use fraud detection, encryption, and tokenization to stop unauthorized transactions. These tools protect businesses and customers from scams.

4. Follow Security Rules and Compliance Standards

Businesses that accept payments must follow security standards like PCI DSS to keep customer data safe. Regular compliance checks and system updates help prevent fraud, avoid legal trouble, and build trust.

5. Keep Your Payment System Updated

Outdated systems can slow down payments, cause errors, or create security risks. Keeping software and security features updated prevents delays and protects transactions.

6. Track and Analyze Payment Data

Tracking payments helps businesses spot trends, fix errors, and improve cash flow. It also makes it easier to manage accounts receivable and avoid late payments. Using payment data helps businesses make better financial decisions.

A well-managed payment process speeds up transactions, makes them more secure, and makes them easier to track. However, manually handling payments takes time and effort.

With Peakflo’s payment processing system, businesses can automate payments, cut financial risks, and improve cash flow. Let’s see how Peakflo helps businesses simplify payments.

How Peakflo Helps in Simplified Payment Processing?

Managing payments manually takes time and leads to mistakes. Late payments, lost invoices, and follow-ups make things harder for finance teams. Peakflo automates payment processing, helping businesses stay on top of cash flow while reducing delays and manual work.

1. Automated Invoice Collections

Tracking payments and reminding customers takes a lot of effort. Peakflo automates invoice collection, payment reminders, and tracking. This means businesses get paid faster without chasing overdue invoices. Finance teams can focus on growth and planning instead of manual follow-ups.

2. Travel and Expense Management

Expense tracking can be confusing. Peakflo automates approvals and payments for travel and business expenses. Finance teams can review and approve spending in real-time, making sure expenses follow company rules. This reduces errors and keeps spending under control.

3. Provides Clear Cash Flow Insights

Unclear cash flow makes planning difficult. Peakflo’s real-time analytics help businesses track payments, find issues, and make smarter financial decisions. With automated vendor payments, businesses can avoid cash shortages and improve stability.

With faster payments, fewer errors, and better control, Peakflo makes managing payments easier. Businesses can reduce manual work, keep records organized, and stay financially secure.

Conclusion

Handling payments can be frustrating. Delayed transactions, lost invoices, and cash flow problems create daily challenges. Manual processes make things worse, leading to errors, extra work, and unhappy vendors. When payments don’t run smoothly, businesses struggle to track expenses and keep records accurate.

A well-organized payment system helps businesses avoid these issues. It ensures payments are made on time, cash flow stays steady, and financial operations run smoothly. However, doing this manually takes too much time and increases mistakes.

Peakflo makes payment processing easier by automating collections, tracking expenses, and providing real-time cash flow insights. Businesses can spend less time chasing payments and more time growing.If payment delays and manual work are slowing you down, request a demo and see how Peakflo can help.

{kind=link}