")

Calculator Template")

: What It Is and How to Calculate")

As a business owner, creating a smooth payment experience for your customers is crucial. To achieve this, it’s important to grasp the distinctions between various payment methods – eCheck vs ACH.

A common source of confusion lies in understanding the difference between ACH payments and eCheck. Although they may appear similar, it’s vital to recognize their key variances before deciding to accept either in your business.

Understanding eCheck

eChecks, short for electronic checks, are a digital version of traditional paper checks used for making payments. Occasionally known as an online or internet check, an eCheck falls under the category of ACH payments. Primarily employed for single transactions, eChecks necessitate verification before processing. They involve transferring funds directly from one bank account to another electronically.

Here is how eCheck works:

Authorization Request: Customers initiate the payment process by providing authorization to the merchant. This can be done through online forms, phone conversations, or signed order forms.

Payment Gateway Setup: Once authorization is secured, users enter the payment gateway to start the transaction process.

Details Submission: Users submit necessary information, including account number, federal tax ID, business details, and address to complete the eCheck transaction.

Payment Confirmation: The funds are automatically withdrawn from the customer’s account and deposited into the merchant’s account. It usually takes 3 to 5 business days for the transaction details to reflect in the account statement. Merchants may incur a small transaction fee for processing eCheck payments.

eChecks offer a quicker and more efficient alternative to traditional checks, allowing for swift electronic transactions between bank accounts.

Understanding ACH

ACH, or Automated Clearing House, facilitates electronic payments between merchants and customers. ACH payments serve as a broad category encompassing any transaction processed through the ACH network.

There are two types: ACH credit and ACH debit, commonly used for bills and utilities. ACH debit involves the merchant pulling the purchase amount directly from the customer’s account, commonly seen in subscription services. Conversely, ACH credit occurs when the payer adds funds to someone else’s account, often used for salary payments.

Here is how ACH payments work:

Authorization Request: Customers give approval (written or verbal) for the payment.

Conversion to ACH: A payment gateway transforms the check into an ACH transaction, and then goes to the merchant’s processor.

Payment Transfer: The ACH transaction is sent to the customer’s bank, validated, and funds are withdrawn from the checking account.

ACH payments take 1 to 2 business days, making them suitable for subscription-based businesses collecting recurring fees.

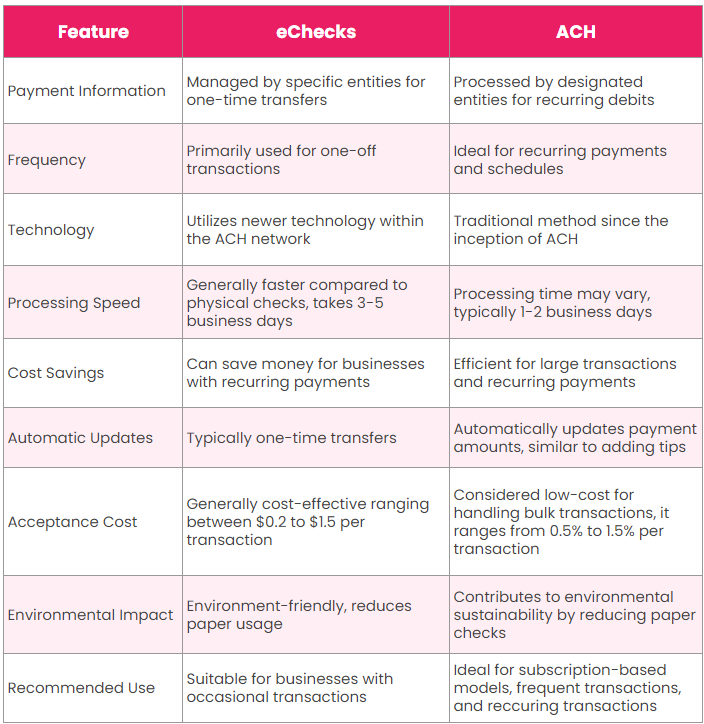

eCheck vs ACH: Understanding the Key Difference

When comparing eChecks to ACH transactions, the crucial distinction lies in who manages payment information and conducts the payments. ACH transactions involve specific entities that utilize banking details from an enrollment form to set up recurring debits from the customer’s bank account. These entities then process payments regularly, whether on a monthly or quarterly basis and can automatically update payment amounts, similar to adding a tip at a restaurant.

Interestingly, eChecks fall under the umbrella of ACH processing, leveraging newer technology introduced after the inception of ACH processing. An eCheck utilizes the ACH network for its payments, typically facilitating a faster one-time transfer between bank accounts compared to physical checks.

For businesses handling recurring monthly payments, incorporating eChecks into your payment processing strategy can lead to cost savings compared to accepting paper checks, debit, and credit cards. The advantages extend beyond cost-effectiveness; eChecks also boast swift processing times. However, it’s advisable to verify specific timelines with your merchant services provider for accurate information.

eCheck vs ACH: Choosing the Right Payment Method for Your Business

When deciding between eCheck and ACH payments, it’s essential to understand the advantages each brings to the table. eCheck, falling under the ACH payment category, emulates traditional checks while incorporating modern data processing and security features. For subscription-based businesses, eCheck and ACH are viable options, streamlining operations and contributing to environmental sustainability by eliminating the need for paper checks.

Opting for electronic alternatives allows customers to set up automatic deductions from their bank accounts, eliminating the hassle of submitting paper checks regularly. ACH payments stand out for large transactions, recurring payments, and direct deposits, providing a seamless experience for customers.

Notably, ACH payments offer an enhanced customer experience, thanks to the convenience of automatic payments. This convenience often leads customers to prefer ACH over traditional payment methods.

Whether you choose ACH or eCheck, both options offer similar advantages, including cost-effectiveness, speed, and heightened security for your business transactions.

Pay Easy with Peakflo

As discussed earlier, eCheck and ACH payments share many similarities, differing mainly in processing time and costs. In both cases, it’s crucial to obtain customer validation before initiating the payment process.

When comparing the two, eCheck stands out for its speed and efficiency, surpassing the traditional paper checks. They also bring enhanced security features, including digital signature processing, authentication, end-to-end encryption, and public-key cryptography, minimizing the risk of fraudulent activities.

Moreover, ACH and eCheck offer user-friendly digital payment options, allowing businesses to choose based on their specific needs and preferences.

Streamline your bill payment process with Peakflo and cut the time in half. Our accounts payable software offers comprehensive automation features, ensuring a swift journey from procurement to payment. Experience the efficiency firsthand by taking a product tour today!

{kind=link}