")

Calculator Template")

: What It Is and How to Calculate")

Accounts receivable insurance, also called trade credit insurance, helps protect your business when customers fail to pay. If a customer doesn’t pay for goods or services, this insurance covers the loss. It keeps your cash flow steady, so unpaid invoices don’t hurt your business.

The cost of this insurance depends on a few factors. These include the risk level of your industry, how reliable your customers are with payments, and your total sales. On average, businesses pay between $1 and $1.50 for every $1,000 in sales. For example, if your company earns $700,000 in a year, your insurance cost could be between $700 and $1,050.

Having this insurance as part of your business plan helps you grow without worrying about customers not paying. It provides financial security and peace of mind.

Before understanding how this insurance works, it’s important to know what it is and why businesses use it. Let’s first look at its meaning and role in business.

What is Accounts Receivable Insurance?

Trade credit insurance, also called accounts receivable insurance, protects your company if customers don’t pay. It covers money owed by customers who can’t pay because of long delays, bankruptcy, or political issues.

What is Receivables Insurance?

Accounts receivable insurance protects your business when customers do not pay their invoices. If a customer fails to pay, the insurance covers most of the unpaid amount. This helps you recover a large part of your loss.

Safeguarding Against Non-Payment by Customers

When customers do not pay on time, your business can face financial trouble. You may struggle to pay your bills or invest in growth. Receivables insurance reduces this risk by ensuring you get paid even if a customer cannot pay.

Function in Preserving the Cash Flow of the Company

A steady cash flow of money is important for running a business. When you know your receivables are protected, you can plan your finances with confidence. Receivables insurance reduces uncertainty and helps keep your cash flow stable.

Receivables insurance is a powerful tool to protect your business from financial stress. It keeps your cash flow strong and allows you to focus on growing your business instead of worrying about unpaid invoices.

Now that you understand why receivables insurance is important, let’s see how it works.

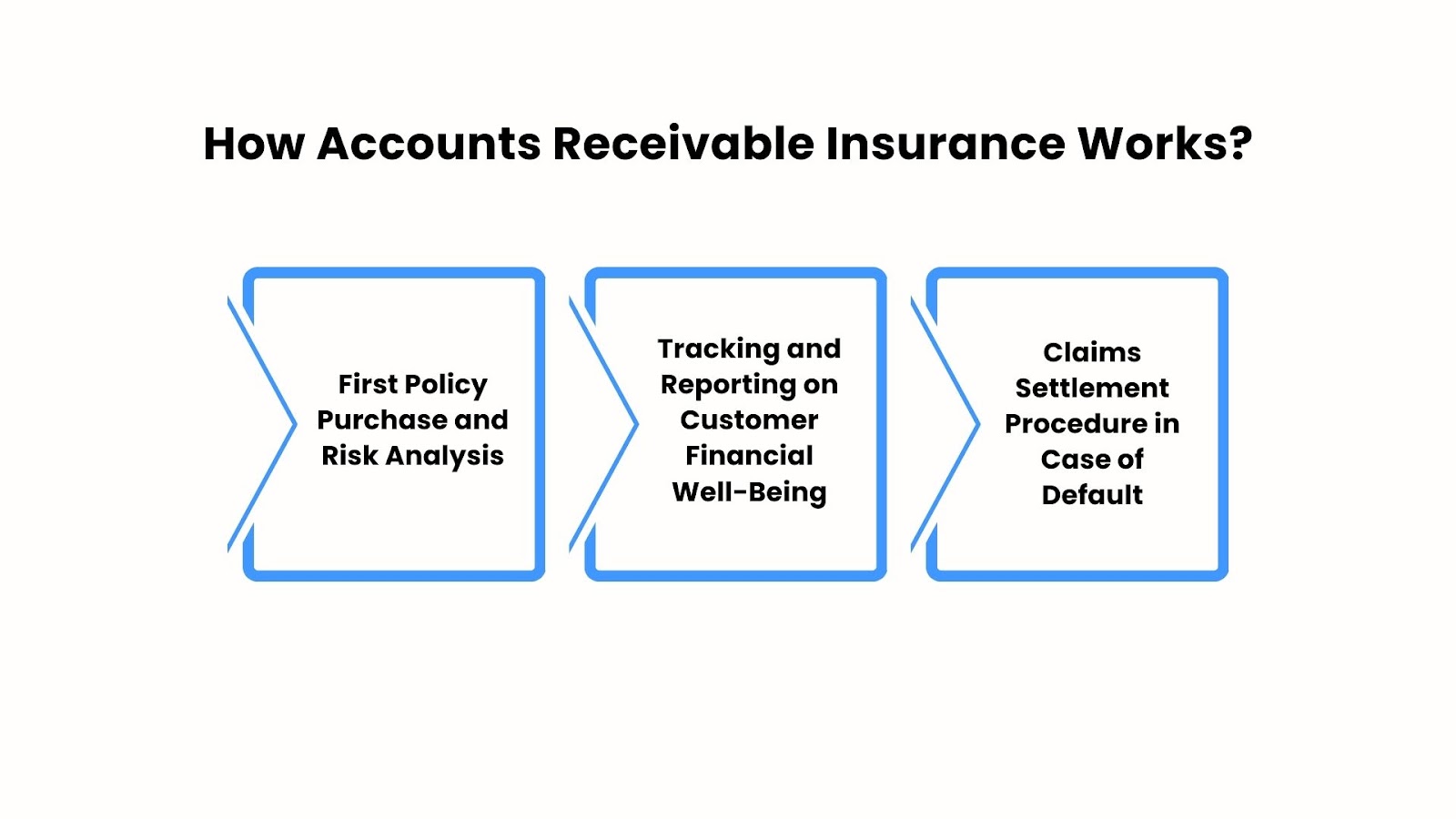

How Accounts Receivable Insurance Works?

Accounts receivable insurance protects your company from monetary losses resulting from unpaid invoices. Here’s how it functions:

- First Policy Purchase and Risk Analysis

- Choosing Coverage: You pick an insurance policy that fits your business needs. You decide which customers and areas you want to insure. The insurer then checks your customers’ financial health by looking at their payment history and financial stability.

- Creditworthiness Assessment of Customers: The insurer sets a credit limit for each customer. This limit shows the highest amount covered based on the customer’s financial situation.

- Ongoing Monitoring: The insurer keeps track of your customers’ financial status. If anything changes, they adjust credit limits to match new risks or improvements.

- Tracking and Reporting on Customer Financial Well-Being

- Regular Reports: You get updates on your customers’ credit status. These reports help you decide whether to offer credit or change payment terms.

- Risk Alerts: If a customer’s financial condition worsens, the insurer sends you a warning. This allows you to act early and reduce potential losses.

- Claims Settlement Procedure in Case of Default

- Reporting a Default: If a customer does not pay on time, you inform the insurer. The insurer checks your claim by reviewing the customer’s credit limit and unpaid amount.

- Receiving Payment: Once approved, the insurer pays you a portion of the unpaid invoice, reducing your financial loss.

Unpaid invoices can disrupt your cash flow and make it hard to pay expenses. This insurance ensures you get paid even if a customer defaults. Steady cash flow keeps your business running smoothly.

Now that we see why it matters, let’s explore how different types of accounts receivable insurance fit various business needs.

Coverage and Types of Accounts Receivable Insurance

Accounts receivable insurance helps your company avoid financial losses when customers don’t pay. If a customer fails to pay due to bankruptcy or insolvency, this insurance keeps your cash flow stable.

Protection Against Non-Payment Due to Bankruptcy or Insolvency

Recovering unpaid debts can be difficult when a customer goes bankrupt or runs out of money. With insurance receivable accounting, your company gets covered for these unpaid amounts. This means you won’t suffer financial losses in such cases.

Various Types of Accounts Receivable Insurance

- Complete Turnover Policies

These policies cover all of your customers’ debts, providing comprehensive protection. This strategy reduces the risk involved in extending credit to multiple customers.

- Single Buyer Policies

Single-buyer policies provide coverage specifically for your high-risk customers. This focused protection ensures efficient management of significant exposures.

- Transactional Insurance

Transactional insurance covers individual deals. It works well for companies that do big but rare transactions. If most of your income comes from single deals, this type of insurance can help.

Using Peakflo to Improve Accounts Receivable Management

Insurance for receivables protects against unpaid invoices. However strong accounts receivable management adds more security. Peakflo is a platform that helps with this. It automates invoicing, sends payment reminders, and keeps records clear. These tools help businesses track payments with AI-powered reports and keep cash flow steady.

Adding accounts receivable insurance to a solid collection process strengthens financial protection. It reduces risks from unpaid invoices and ensures a steady income.

This type of insurance does more than protect against losses. It also helps businesses offer credit safely, predict cash flow, and improve financing options. These benefits support business growth and stability.

Benefits of Accounts Receivable Insurance

Accounts receivable insurance has many benefits for your business. It helps you protect your money and grow safely.

- Increase Sales by Safely Extending Credit

With this insurance, you can give customers more time to pay without worrying about losses. People like buying from companies that offer credit, so this can help you sell more. If a customer doesn’t pay, the insurance covers most of the loss, saving you money.

- Improve Your Credit Terms

You can give customers better payment options than your competitors. Since the insurance lowers the risk of unpaid bills, you can extend credit with confidence. This not only attracts new customers but also builds strong relationships with existing ones.

- Improve Cash Flow Forecasting

Even if some customers don’t pay on time, this insurance helps keep your cash flow stable. Your business remains financially secure, making it easier to plan for the future.

- Get Better Lender Financing Terms

Lenders trust insured receivables more than uninsured ones. This means banks might offer you lower interest rates and higher loan amounts. With better financing, you can grow your business faster.

Using accounts receivable insurance protects your business and helps it expand. Managing this insurance well is key to getting the most benefits. The next section will cover the best ways to handle accounts receivable insurance efficiently.

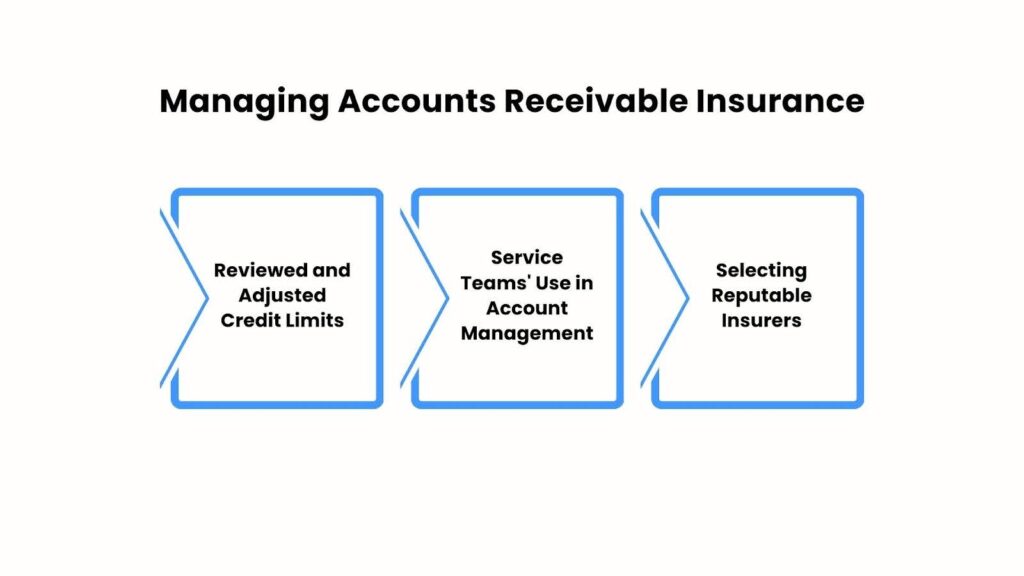

Managing Accounts Receivable Insurance

Several essential procedures are necessary for managing accounts receivable insurance effectively.

- Reviewed and Adjusted Credit Limits

To lower the risk of nonpayment, check your customers’ credit strength often. Insurance companies study their financial health and give them risk ratings based on detailed data.

For example, Allianz Trade reviews buyer and national risks to help with credit choices. By keeping track of your customers’ finances, you can adjust credit limits in advance and reduce possible losses.

- Service Teams’ Use in Account Management

Use your insurer’s service team expertise to manage accounts efficiently. These teams assist with tasks such as determining credit limits and managing claims.

Companies set up special teams to help people with their policies. These teams quickly solve problems and answer questions. Working with these teams improves your ability to manage accounts receivable effectively.

- Selecting Reputable Insurers

Pick insurance companies that are known for handling claims well. A good insurer does more than just provide coverage. They also help manage credit limits and check if customers can repay what they owe.

Some insurers offer full services designed for your business. They may provide credit checks and assign teams to manage your accounts. Choosing a well-known insurer ensures you get reliable support throughout your policy.

Adding these steps to your insurance receivable accounting can make financial risk management much stronger.

Managing accounts receivable insurance effectively is essential, but how much does it cost? Businesses must weigh these expenses against the potential financial risks of unpaid invoices. Let’s explore the factors that affect policy pricing and affordability.

Cost Considerations for Accounts Receivable Insurance

- Influence of Industry, Customer Base, and Claims History

Several factors influence the cost of premiums for insurance receivable accounting. A major factor is your industry; higher default-risk sectors might have higher premiums. The type of customers you have also matters.

The risk level of your business can affect insurance costs. If you work with customers who have poor credit or operate, your insurance premiums may go up. Your claims history also plays a role. If your company has filed many claims in the past, insurers may see you as high-risk and charge higher premiums.

- Comparison of Costs versus Potential Unpaid Invoice Losses

It’s important to weigh the cost of insurance against the risk of unpaid invoices. Typically, insurance premiums range from 0.2% to 1% of your total accounts receivable.

For instance, if your business has $1 million in receivables, your premium might be between $2,000 and $10,000 per year. If a major customer fails to pay, the financial hit could be much greater than the insurance cost. That’s why many companies see this insurance as a smart investment.

- Factors Affecting Policy Pricing and Affordability

Policies for high-risk accounts may have different costs than those covering all accounts. The size of your business also plays a role. Companies with higher sales often get better rates.

The type of policy you choose affects the price. For example, policies with cancelable limits usually cost more than those with non-cancelable limits. Insurers also give better rates to businesses that have many different customers, reducing risk.

Every business must decide if this insurance is worth the expense. The next section will help you determine if the benefits outweigh the costs.

Is Accounts Receivable Insurance Worth the Investment?

- Evaluation of Financial Implications of Non-Payment

When customers don’t pay on time, your business can struggle. You may not have enough cash to cover daily expenses. This can also make it harder to grow your company.

Accounts receivable insurance helps by covering a large part of unpaid invoices. This protects your business from financial trouble and keeps your cash flow steady.

- Weighing Costs against the Benefits of Secured Revenue

It’s important to compare the cost of insurance receivable accounting with its benefits. You have to pay a small fee, usually less than 1% of your sales. But in return, you get protection against unpaid bills.

With this safety net, you can plan for growth without worrying about bad debt. Your cash flow remains stable, giving you confidence to invest in new opportunities.

- Potential Impacts on Business Growth and Stability

This insurance can have a big impact on your company’s future. It reduces the risks of selling to new customers or entering new markets. You can expand without fearing financial loss.

It also improves your company’s creditworthiness. This means banks and lenders may offer you better loan terms. Strong finances help your business grow and stay stable over time.

Using tools like Peakflo can make things even better. Peakflo helps you get paid faster by automating invoices and payment reminders. This reduces the chances of late or missed payments.

How Peakflo’s Accounts Receivable Solution Can Help You?

Using Peakflo for accounts receivable can improve your finances. It helps in invoicing and payment reminders, helping businesses collect payments 10–15 days faster. Let’s explore how Peakflo makes managing accounts receivable easier.

- Monitoring Unpaid Amounts: Peakflo helps you see which invoices are unpaid, which customers owe money, and how long payments are overdue. This makes it easy to track payments and focus on the most urgent accounts.

- Automating Reminders for Payments: Peakflo allows you to customize and set payment reminders for overdue payments. This reduces delays, improves cash flow, and saves businesses time.

- Flexible Payment Options: Peakflo allows businesses to provide multiple payment options. Customers can pay using bank transfers, credit cards, or digital payment methods. This makes it easier for them to complete payments on time.

- Simplifying the Invoicing Process: You can create and send invoices directly from Peakflo. It ensures invoices are clear, accurate, and mistake-free. Whether you use templates or customize them, the process is fast and simple.

- Financial System Integration: Peakflo connects easily with accounting software and financial tools. This keeps financial records accurate and ensures every payment is recorded and reconciled automatically.

- AI-powered Reports: Peakflo gives you instant access to reports on accounts receivable. These reports show payment trends, overdue invoices, and cash flow details. With this data, businesses can make smarter financial decisions.

- Decreasing AR Disputes: Peakflo keeps records of invoices, payments, and customer interactions in one place. This makes it easy to resolve disputes quickly and avoid major issues.

- Bad Debt Risk Management: Peakflo helps businesses spot payment issues early. If a customer struggles to pay, businesses can take action, like offering payment plans or stopping further credit. This reduces financial losses.

- Improving Relationships with Customers: Peakflo ensures businesses get paid without harming relationships. It sends reminders and keeps communication clear. This builds trust and long-term customer loyalty.

Conclusion

Accounts receivable insurance helps keep your business financially strong. It protects you if customers don’t pay, ensuring a steady cash flow.

With this insurance, you can offer credit to customers without worrying about big losses. It also helps you make smart choices about who gets credit. Insurance providers check your customers’ financial health, so you can make better decisions.

This protection lowers the risk of unpaid invoices. It also gives you more confidence when extending credit, helping your business grow.

Using Peakflo in your accounts receivable process can improve your finances. It helps in invoicing and payment reminders, helping businesses collect payments 10–15 days faster.

Peakflo’s reminders have saved companies over 3,000 work hours. This boosts productivity and helps collections teams use their time wisely. Request a demo with Peakflo today!

{kind=link}